Why there are more data centers on paper than physically available

The Phantom Data Centre Problem : Why the world's most ambitious technology buildout exists largely on paper and what that gap means for the AI era.

This article is based on research compiled from Goldman Sachs, DC Byte, Sightline Climate, McKinsey, Bessemer Venture Partners, CBRE & ITIF.

The Problem

Published numbers of data centers don’t add up

Every announce of new data center creates a fascade of growing AI economy where investors pump in capital in these ventures. Open any technology publication today and you will find announcements of staggering scale of a half-trillion-dollar campus in Texas, a two-gigawatt facility the size of part of Manhattan, server farms that will consume more electricity than entire cities. The data centre industry has never looked more ambitious or more crowded with press releases.

; US BLS (2026). License: CC BY.")

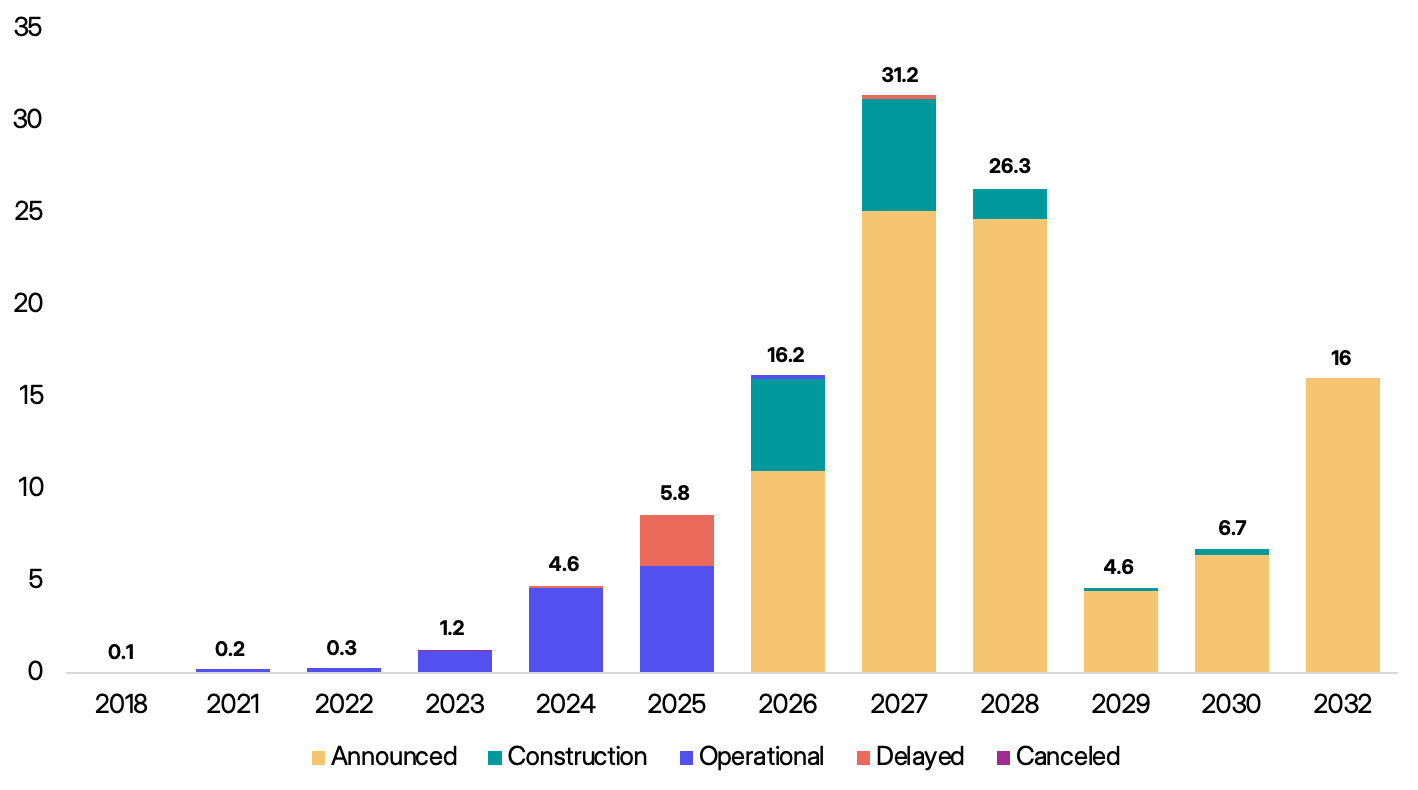

But look past the headlines and a troubling pattern emerges. Analysts at Sightline Climate are currently tracking 190 GW of capacity across 777 large data centres and AI factories announced since January 2024. Out of the facilities due to come online in 2026, only around 5 GW is confirmed under active construction. The typical construction timelines can be 12–18 months. 1

In other words, the majority of the world’s most-discussed infrastructure boom exists, for now, primarily on paper.

"The market is not cooling. It is overcommitted and underdelivered. Projects are being leased before construction starts, but grid delays and permitting hold-ups are pushing delivery further out. This isn't a demand problem. It is a development bottleneck."

- Colby Cox, Managing Director Americas, DC Byte.

DC Byte's 2025 Global Data Centre Index quantifies the divergence with striking precision: committed supply has increased more than six times since 2019, while live capacity has grown at a far slower pace. This is not a rounding error but there is a structural disconnect between what the industry declaration and what is built2.

Agitate

Reasons that keeps this gap growing

To understand why so many proposed data centers and capex exist on paper. This is due to a number of factors. There is a disconnect during the press release and the construction of new data centers. These are not isolated problems. They tend to arrive together and each problem compounds on the other.

Grid Connection: It takes up to 12-18 months to construct new data centers. Connecting them to the electrical grid currently takes five to seven years. Hence there is a backlog of data centers that can not be connnected to national grids. Grid-power capacity in most major US markets is already committed through 20303

Construction permit:Between March 2024 and 2025, 16 data centre developments were delayed or denied due to permitting restrictions. Permitting accounted for 29% of all milestone change requests for projects under construction, according to PJM grid operator data.[34]

Equipment Shortages: Supply chain issues for electrical back-up generators, cooling system account for the delays. Electrical sub-station transformer lead times averaged around 140 weeks in 2023, rose to 150 weeks in 2025, and now exceed 160 weeks in 2026. Data center constuctors are competing directly with utilities providers for the same limited pool of electrical components.[4]

Community oppostion: Most residences living close to data centers, heavily oppose these huge construction despite the promise of jobs. At least 188 local activitist opposition groups are now active across 40 US states. Data centre project cancellations more than quadrupled from 6 in 2024 to 25 in 2025. Public concern over water use, grid strain, and environmental impact has become a genuine material risk.56

Capital Constraints: This might be surprise. These hyperscale can not afford to expontially build these data centers with debt. New data center deal volume fell more than 40% between Q3 and Q4 of 2025. Out of the 240 GW planned, only one-third is actually under construction. Even hyperscalers have begun cancelling or pausing leases, with Microsoft alone withdrawing "a couple of hundred megawatts" of commitments.7

Strategic Facade: Many announcements are intentionally speculative: some data center developers launch multiple projects in parallel and build only those that secure power and permits fastest. Announcements serve investor relations and competitive positioning as much as they do operational planning. [1]

Environmental Concerns: Data centers present severe environmental challenges across energy, water, and local ecosystems. Large data centers can consume up to 5 million gallons of water daily equivalent to the footprint of a town of 50,000 people. Sound pollution of continuous humming from rooftop HVAC systems and massive industrial fans can reach internal levels of 96 decibels. Externally, this noise creates a persistent low-frequency hum that disrupts sleep of residence. E-waste acceleration with the hardware lifecycles of cloud computing add a hidden layer of chemical and physical waste to the environment such as the PFAS “forever chemicals“ accumulate permanently in the local soil and water.

The track record bears the truth

Goldman Sachs Research, drawing on granular facility-level data from Aterio that incorporates satellite imagery and permitting progress, found that historically only about 72% of data centres scheduled for activation within the following four quarters actually come online on time. The further out a project is scheduled, the worse that ratio becomes.8

Bessemer Venture Partners, points out that out of the 110 data centre projects slated to come online in 2025, more than a quarter were delayed due to power, permitting, and construction constraints. [3]

"What looks viable on paper usually breaks down on power, permitting or labor, and sometimes all three."

— Brennan Church, Director of engineering, procurement and construction at data center developer Hut, New York Build Conference 2026 [5]

The problem is not limited to any single geography. Across Europe the equivalent strain is also exist, particularly in London, Dublin, and Frankfurt, where low vacancy rates, planning restrictions, and constrained power availability are slowing delivery. In Southeast Asia, the volume of live capacity is falling behind the rate of announcements even in high-growth markets. [2]

Construction costs are rising on top of all this: Turner & Townsend’s 2025 Data Centre Construction Cost Index shows a 5.5% increase per watt for traditional cloud data centres, with AI-specific facilities facing cost variables that are still too early to benchmark globally. The three most expensive markets — Tokyo, Singapore, and Osaka now cost upwards of $14 per watt to build. [9]

Solution

Power certainty is the Primary filter criterion

Grid capacity has displaced fibre connectivity, land cost, and tax incentives as the first filter in serious site selection. DC Byte’s regional analysis shows that markets with predictable power supply and coordinated planning frameworks deliver capacity more consistently, with smaller gaps between announced, committed, and live supply. Norway’s qualified supply grew at a 43% five-year CAGR since 2019; Finland added more than 1,400 MW of IT load across 2023 and 2024 alone both markets benefiting from stable grid environments. [2]

Sites offering power access within 18 to 36 months are among the most sought-after assets in the market. Data center developers who can demonstrate grid certainty, not just construction plans, command premium positioning with anchor tenants. 10

On-Site power is a strategic approach

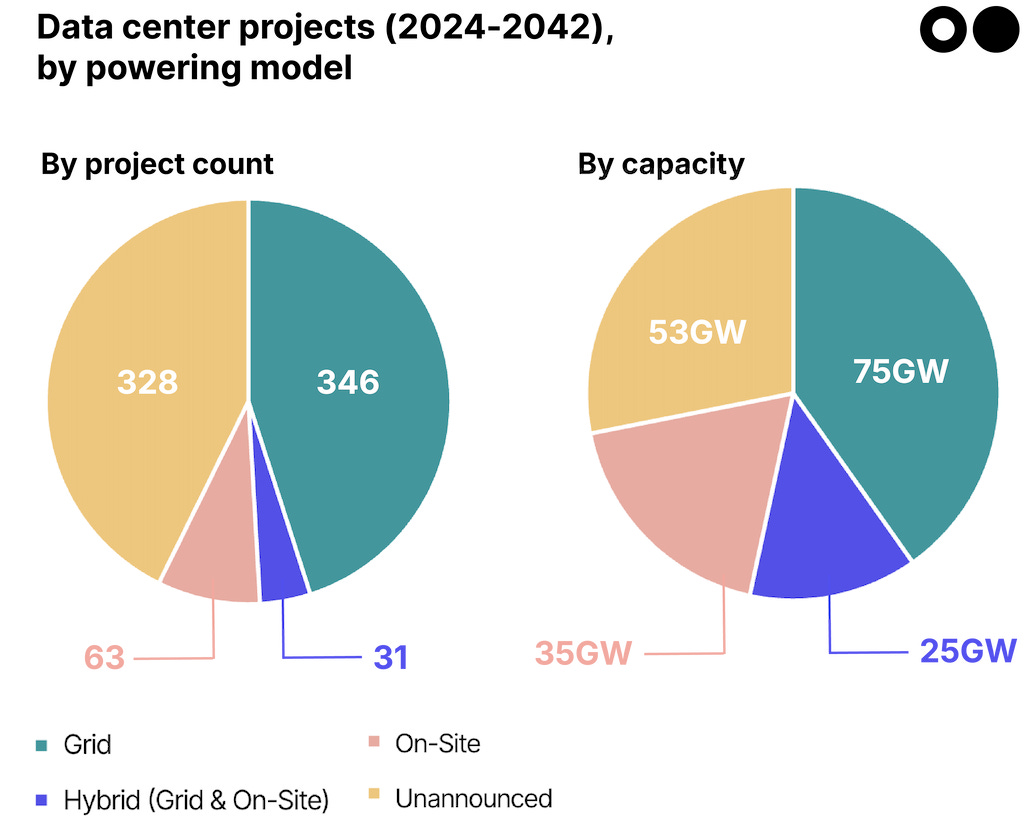

Hyperscalers are increasingly bypassing the public grid entirely for AI training capacity. Hybrid systems combining batteries with gas turbines, solar-plus-storage. In Google’s case, investment in nuclear reactor partnerships are becoming mainstream. The US Department of Energy issued a directive in October 2025 proposing federal jurisdiction over new loads above 20 MW, aiming to create standardised, faster approval pathways for projects willing to accept occasional curtailment during grid stress events. [4, 11]

Execution capability is now a competitive moat

Bain & Company’s 2030 global data centre forecast identifies a decisive shift underway: the early scramble of AI-driven demand is giving way to a more disciplined, execution-focused phase. Data center developers who have already secured power, land, and permits are in a position to lead; those who have not may be forced to pause or substantially rework plans as grid timelines extend. [12]

“As demand continues to grow, the real differentiator is no longer how much capacity is announced, but how much can actually be delivered. Power availability, planning certainty, and realistic timelines are now what separate markets that scale from those that stall.”— Siddharth Muzumdar, SVP of Research, DC Byte [2]

Customers particularly large enterprises and cloud buyers are increasingly prioritising partners who can offer contractual certainty around timelines and activation, not just headline capacity numbers. This is reshaping how capital is deployed: investors are applying more rigorous deliverability, durability, and adaptability screens before committing, rather than treating announced pipeline as a reliable proxy for future supply. [2, 13]

For Investors and Analysts: Read Beneath the Announcement

No one know with certainty if we are in an AI bubble compared with the DotCom bubble where there were speculative investing, reckless capex expenditure, investing in business model that were not profitable such as notable unprofitable “paper” business Pet.com. We at BE Invested, believe that if there will be an AI bubble in the future. This will be initial indication point.

For investors, a practical implication for anyone tracking this space whether allocating capital, procuring capacity, or modelling energy demand is that announced figures require heavy discounting and due diligence. Goldman Sachs’ research cautions explicitly that ambitious construction schedules carry meaningful uncertainty in both directions, and notes that elevated capital spending could compress timelines while delays and cancellations could reduce activated capacity well below current projections. [8]

The ITIF, writing in April 2026, offered the clearest summary of the gap: Out of 240 GW of planned construction, only one-third is actually being built. The Stargate project where OpenAI’s flagship $500 billion commitment in Texas. Stargate itself is stalled amid disputes between partners. Announcements, in the current environment, are better understood as options than as commitments. [7]

The data centre industry will almost certainly build a remarkable amount of new infrastructure over the next five years. McKinsey projects $6.7 trillion in cumulative global capital expenditure between 2025 and 2030 to meet demand, with $5.2 trillion dedicated to AI-specific infrastructure. [13] But the gap between what gets announced and what gets built will remain large and understanding why that gap exists is the prerequisite for navigating the AI infrastructure era with any degree of analytical clarity.

[Sightline Climate, Data Center Outlook, February 2026. sightlineclimate.com

DC Byte, 2026 Data Centre Outlook: Top Five Trends & Global Data Centre Gridlock, January 2026 / August 2025. dcbyte.com

Data Center Knowledge, Why AI Data Center Projects Face Years of Delays After Approval, June 2026. datacenterknowledge.com

Construction Dive, What’s Stalling Data Center Projects?, April 2026. constructiondive.com

Cargoson, Number of Data Centers by Country, November 2025. cargoson.com

Goldman Sachs, US Data Center Power Demand Projected to Double by 2027, 2026. goldmansachs.com

Turner & Townsend, Data Centre Construction Cost Index 2025. turnerandtownsend.com

Power Engineering, Data Centers Shattered Records in 2025. So Why Is Construction Slowing Down?, March 2026. power-eng.com

Hanwha Data Centers, Data Center Grid Limitations: The Power Bottleneck, February 2026. hanwhadatacenters.com

McKinsey, The $7 Trillion Race for AI Data Center Infrastructure, March 2026. mckinsey.com

Great article man, actually interesting

Subscribed, would love to have you along too🙂🙌