Business breakdown about Sandisk: AI Momentum vs Cyclical Gravity

BE Invested Labs research shows why one of the hottest AI storage stocks may be both a great business and a dangerous valuation at the same time. (Read time is 16 minutes)

Growing up in age of Nintendo DS2, and Nikon digital camera, having a SanDisk memory stick is a must for using these devices. However, we are looking at SanDisk from the lens of investors.

A few days ago, we launched BE Invested Labs with a simple mission: help everyday investors move from scattered market information to structured research.

Not more noise.

Not another dashboard.

Not another place where you open ten tabs, read five opinions, check two YouTube videos, and somehow end up less clear than when you started.

The goal is different.

The goal is to take a stock, structure the research, pressure-test the thesis, show both the bull case and the bear case, and help the investor understand what is really driving the opportunity.

Today, we are using Sandisk Corporation, ticker SNDK, as a live example. And it is a perfect case study.

Prefer to listen?

We also generated an AI audio briefing from the BE Invested Labs platform for this Sandisk report. You can listen to the discussion first, then read the full research breakdown below.

Audio briefing generated by BE Invested Labs from the Sandisk institutional research report.

Because Sandisk is exactly the kind of stock that can confuse investors. On one side, the story is powerful. AI data centers need more storage. Enterprise SSD demand is surging. NAND flash pricing has tightened. Revenue has exploded. Margins have expanded. The balance sheet has improved. The stock has gone almost vertical.

On the other side, memory is one of the most cyclical areas in semiconductors. These businesses can look unbeatable at the top of the cycle and broken at the bottom. Profitability can swing violently. Pricing can reverse. Valuation multiples can compress. Investors who buy the narrative late can get punished, even if the underlying company is genuinely strong.

That is why Sandisk is not a simple “AI winner” story.

It is more interesting than that.

It is a battle between AI momentum and cyclical gravity.

And this is exactly where structured research matters.

Why Sandisk Is Suddenly Back In The Market Conversation

Sandisk became a standalone public company again after its separation from Western Digital in February 2025. The company is a pure-play flash memory and storage business, focused on NAND flash memory products, including enterprise SSDs, consumer storage, and edge devices. Since the spin-off, Sandisk has moved from being a forgotten component inside a larger storage company to becoming one of the most talked-about AI infrastructure stocks in the market. Reuters and other outlets have reported that Sandisk’s shares have surged dramatically since the spin-off, supported by AI-driven demand for high-performance data storage. (Reuters).

The reason is simple: AI does not only need GPUs.

AI needs memory.

AI needs storage.

AI needs data to be stored, moved, retrieved, trained on, and processed at scale.

That is where NAND flash becomes important. NAND is non-volatile memory, meaning it stores data even when power is removed. It is the technology behind many SSDs and flash storage products. In the AI data centre world, high-performance SSDs are increasingly important because modern AI workloads need fast access to massive amounts of data.

Sandisk’s recent numbers show how quickly the market has changed. In its fiscal third quarter, the company reported revenue of $5.95 billion, far ahead of analyst expectations, with adjusted earnings of $23.41 per share. Reuters reported that the company guided for the following quarter to revenue between $7.75 billion and $8.25 billion, also ahead of consensus expectations. (Reuters)

That is not normal growth. That is a step-change. But the BE Invested Labs report did something important: it did not stop at the growth story.

It asked a harder question:

How much of this good news is already priced in?

What The BE Invested Engine Concluded

The BE Invested Labs institutional research engine initiated coverage on Sandisk with a Neutral rating. That may surprise people who only look at the revenue growth, the AI narrative, or the share price momentum.

But this is exactly why the report is useful. A shallow AI summary could easily say:

“Sandisk is benefiting from AI demand. Revenue is growing. The stock is strong.”

That is not research. That is a headline!

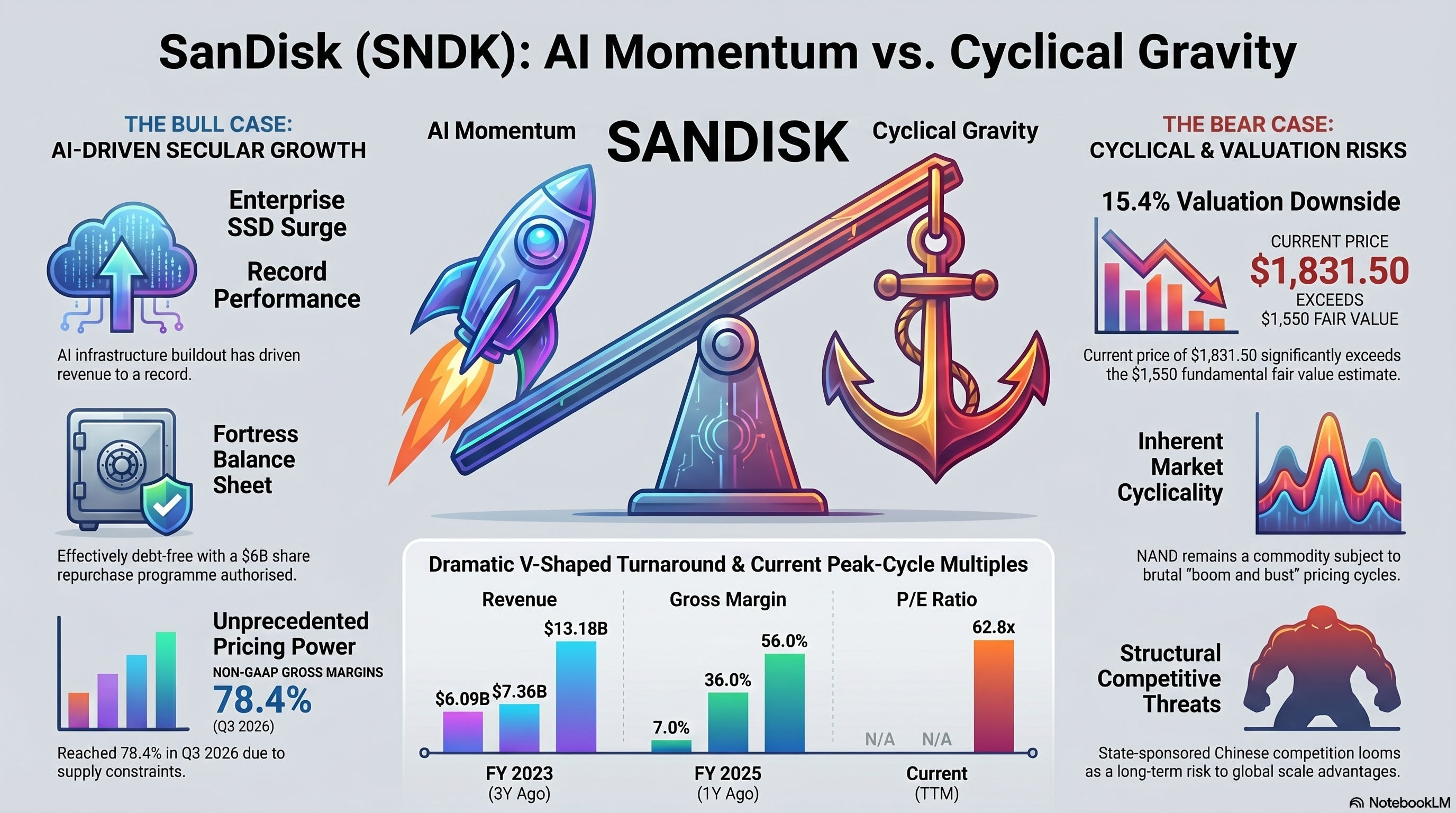

Our research engine went deeper. It concluded that Sandisk is executing extremely well, but that the stock’s valuation already reflects a near-perfect version of the future. The report estimated fair value around $1,550 per share, compared with a current price used in the report of $1,831.50, implying roughly 15.4% downside to the fair value estimate. The report also modelled a bull case around $2,200, a base case around $1,500, and a bear case around $900, showing a wide distribution of possible outcomes.

That wide range matters. It tells us the stock is not easy.

Sandisk could continue winning if AI demand remains strong, NAND pricing stays tight, customers sign long-term contracts, and margins remain elevated. But if the market begins to believe this is a cyclical peak rather than a permanent new level of profitability, the downside could be painful.

That is the point. A good research platform should not just confirm excitement.

It should structure uncertainty.

The Bull Case: AI Has Changed The Storage Market

The bull case for Sandisk is not weak. In fact, it is very compelling.

The core argument is that AI has created a structural change in storage demand. Large language models, AI agents, enterprise automation, cloud workloads, and hyperscale data centres require enormous amounts of high-speed storage. That means demand for enterprise SSDs and NAND flash products may remain stronger for longer than historical cycles would suggest.

Reuters reported that Sandisk has signed five long-term customer agreements, with three of those agreements worth at least $42 billion. These agreements are designed to help reduce the extreme boom-and-bust dynamics that have historically defined the memory business. CEO David Goeckeler told Reuters that the company wants more consistent and predictable economics, with contract structures that include financial commitments from customers. (Reuters)

That is important because memory companies have historically suffered from weak visibility. Prices rise, companies add capacity, supply eventually catches up, prices fall, margins collapse, and the cycle repeats. If Sandisk can genuinely move more of its revenue into long-term agreements with financial commitments, that could change the quality of the business.

The bull case rests on four pillars.

First, AI infrastructure demand remains strong. Cloud providers, hyperscalers, and enterprise customers continue spending heavily on data centres, and storage becomes a critical bottleneck.

Second, NAND supply remains disciplined. If competitors such as Samsung, SK Hynix, Micron, and Kioxia do not flood the market with new capacity, pricing can stay stronger for longer.

Third, Sandisk shifts more of its mix toward enterprise and data centre SSDs. This matters because enterprise products typically carry better margins than lower-end consumer storage.

Fourth, Sandisk’s balance sheet and capital return strategy improve shareholder outcomes. The company has announced a $6 billion share buyback, which could support earnings per share if executed at reasonable valuations. (Reuters)

In this version of the future, Sandisk is not simply a cyclical memory company. It becomes a premium AI infrastructure supplier with better pricing visibility, higher margins, and a more durable earnings base.

The Bear Case: Memory Cycles Have Not Disappeared

But here is where investors need to be careful.

The bear case is not that Sandisk is a bad company.

The bear case is that Sandisk is a very good cyclical company being valued like a structurally superior compounder.

There is a big difference.

The memory industry has a long history of booms and busts. When demand rises and pricing improves, margins expand rapidly. But when supply catches up, pricing can fall brutally. In capital-intensive industries, today’s shortage often becomes tomorrow’s oversupply because every competitor sees the same high prices and has an incentive to add capacity.

That is the old gravity of the memory business.

The BE Invested Labs report captured this tension well. It described Sandisk as having powerful AI-driven near-term momentum, but also highlighted that the business remains tied to NAND pricing, industry supply discipline, and capital intensity. The report flagged the risk that current profitability may represent peak-cycle conditions rather than a new permanent baseline.

This is why the valuation matters.

At the time of the BE Invested report, Sandisk was trading at valuation levels that looked stretched compared with traditional semiconductor memory peers. The report cited a trailing P/E above 62x and EV/EBITDA around 44.5x, while also noting that forward multiples depend heavily on whether analysts are right about sustained earnings power.

That creates a problem. If Sandisk keeps beating expectations, the stock can keep working. But if investors begin to question the durability of the cycle, the multiple can compress quickly.

This is one of the most dangerous situations in investing:

a real business, with real growth, at a price that already assumes too much goes right.

The Financial Turnaround Is Real

One of the strongest parts of the Sandisk story is that the financial turnaround is not imaginary.

This is not just a stock moving on vibes.

Revenue has genuinely accelerated. Profitability has improved. AI-related demand is showing up in reported numbers. The company’s fiscal third quarter revenue of $5.95 billion represented a major beat versus expectations, while adjusted earnings of $23.41 per share also beat analyst estimates by a wide margin. For the following quarter, Sandisk guided revenue between $7.75 billion and $8.25 billion, again above consensus. (Reuters)

The BE Invested report also highlighted the longer-term revenue recovery. It showed revenue falling sharply during the previous NAND downturn, before recovering through fiscal 2024 and fiscal 2025, and then accelerating strongly on a trailing twelve-month basis. This is the V-shaped recovery visible in the report’s financial section.

But this is also where investors must think carefully.

In a cyclical industry, the income statement can look terrible at the bottom and unbelievable at the top. The same company can swing from losses to record profits in a short period because pricing, utilization, and operating leverage all move together.

That is why the question is not only:

“Are the numbers good?”

The question is:

“Are these numbers sustainable?”

That is a more difficult question. And it is the question the market as a both weighing and voting machine is now trying to answer.

The Balance Sheet Gives Sandisk Flexibility

One area where the report was clearly positive is the balance sheet.

The BE Invested analysis described Sandisk’s balance sheet as a “fortress,” noting a significant cash position, minimal debt, and a net cash position after debt reduction. The report also highlighted management’s capital allocation decisions, including the planned buyback.

That matters because cyclical businesses need balance sheet strength.

When a cycle turns, weak balance sheets become dangerous. Companies with too much debt can be forced to cut investment, issue shares, sell assets, or refinance under pressure. Companies with strong balance sheets have more options. They can continue investing through downturns, repurchase shares when valuations are attractive, and avoid being forced into bad decisions.

Sandisk’s current balance sheet strength is therefore a real positive.

But again, balance sheet strength does not make valuation risk disappear. A strong balance sheet can help a company survive a downturn. It cannot guarantee that investors who paid too high a price will avoid losses.

Management Is Trying To Change The Industry Model

One of the most interesting parts of the Sandisk story is management’s attempt to reduce cyclicality through long-term agreements.

This is important because the historical memory model has been painful for shareholders. Customers often negotiate aggressively, supply/demand changes quickly, and prices can move sharply. Sandisk’s long-term supply agreements are an attempt to bring more stability to a business that has traditionally lacked it.

The company has said these agreements include financial commitments and structures intended to prevent customers from simply walking away when pricing weakens. Reuters reported Goeckeler’s comments that Sandisk is trying to escape the “boom-bust cycle” and create more consistent economics. (Reuters)

If this works, it could justify a higher valuation multiple.

But investors should not assume success too quickly.

The bear case is that long-term agreements help, but do not fully eliminate the commodity nature of NAND. If the market becomes oversupplied, customers may still push back, competitors may discount, and the market may rediscover that memory is still memory.

This is why the BE Invested report framed management’s narrative carefully. It recognised the strategic importance of long-term agreements, but did not accept the idea that Sandisk has completely escaped cyclicality.

The Moat: Strong Technology, Narrow Industry Protection

The report’s moat assessment was also useful.

It did not call Sandisk a wide-moat business. It rated the moat as narrow, despite recognising the company’s strong intellectual property, manufacturing scale, technology base, and customer relationships.

That may feel harsh, but it is reasonable.

Sandisk has real advantages. It has decades of flash memory experience, a recognised brand, a manufacturing partnership with Kioxia, deep customer relationships, and exposure to mission-critical storage demand.

But the industry structure is difficult.

There are well-funded competitors. Technology cycles move fast. Manufacturing is capital intensive. Pricing is volatile. And state-supported competition, especially from China, remains a long-term risk.

In other words, Sandisk may be a very strong player in a very hard industry.

That is not the same thing as being a dominant software company with recurring revenue, low capital intensity, and high switching costs.

This distinction matters because investors often confuse technological importance with investment quality.

A product can be essential, but the economics can still be cyclical.

A company can be strategically important, but the stock can still be overvalued.

A business can be real, but the market can still price it too aggressively.

That is exactly the kind of nuance BE Invested Labs is built to surface.

Valuation: The Hardest Part Of The Sandisk Story

The BE Invested report valued Sandisk using a mix of discounted cash flow analysis, peer comparison, and scenario analysis. The base DCF value was around $1,500 per share, with a probability-weighted value around $1,530 to $1,550 depending on the scenario mix. The report’s bull case was $2,200, while the bear case was $900.

Those numbers tell the story better than any headline.

The upside exists, but it is not massive relative to the downside.

In the bull case, AI demand remains strong, NAND pricing stays tight, margins remain elevated, and Sandisk uses cash flow to repurchase shares. In that world, the stock can still move higher.

In the base case, the AI demand surge continues for a while, but margins eventually normalise and the market begins to apply a more reasonable multiple.

In the bear case, the market realises this was another memory cycle. NAND prices fall, margins compress, the multiple de-rates, and investors who bought late experience serious downside.

That is the risk/reward issue.At lower prices, Sandisk could be a very attractive cyclical growth opportunity.

At stretched prices, it becomes a much harder decision.

This is why the report’s conclusion was Neutral rather than Bullish. It was not saying the business is weak. It was saying the price matters.

And price always matters.

What This Shows About BE Invested Labs

This is the real reason we wanted to publish this research.

Not because Sandisk is trending. Not because AI storage is exciting.

Not because we want to chase the hottest ticker.

We wanted to show the type of work BE Invested Labs is designed to do.

The platform does not simply summarize a stock. It builds a structured research framework around it. It looks at the business model, the moat, the bull case, the bear case, the financial trajectory, the balance sheet, management, valuation, and scenario risk.

Most importantly, it can hold two ideas at once.

Sandisk can be a strong company. Sandisk can also be expensive.

AI demand can be real. The memory cycle can also still matter.

Management can be right about structural improvement.

The market can still be overpaying for that improvement.

That is how investment research should work. Not based on FOMO or hype.

Our View

Our view is broadly aligned with the engine’s conclusion.

Sandisk is one of the most interesting AI infrastructure names in the market right now. The company is benefiting from real demand, real pricing power, and real financial momentum. Its recent results and guidance show that AI-related storage demand is not just a narrative; it is flowing through the numbers.

But the stock is also pricing in a lot of good news.

For investors, this creates a very specific problem. The question is not whether Sandisk is important. It clearly is. The question is whether the current price offers enough margin of safety given the cyclicality of NAND, the intensity of competition, and the risk that today’s extraordinary margins eventually normalise.

That is why Neutral makes sense. Not because the story is weak.

But because the valuation is demanding. If Sandisk continues executing, there may still be upside. But if the market begins to doubt the “AI super-cycle” narrative, the downside could be much larger than investors expect.

This is not a stock to approach casually. It requires monitoring. Specifically, investors should watch:

NAND contract pricing. Data centre revenue growth. Gross margin sustainability. Competitor capital expenditure. Long-term customer agreement quality. Buyback execution. Inventory levels. Management language around supply discipline.

Those are the signals that will tell us whether Sandisk is becoming a structurally better business, or whether we are simply witnessing a powerful cyclical peak.

Final Thought

Sandisk is a perfect example of why modern investors need better research tools.

The story is too important to ignore, but too complex to judge from headlines alone.

If you only look at the AI narrative, you may become too bullish.

If you only look at memory cyclicality, you may become too bearish.

If you only look at the stock chart, you may arrive too late.

If you only look at valuation multiples, you may miss the structural change.

The truth sits somewhere in the tension.

That is what BE Invested Labs is trying to help investors find.

Not certainty. Clarity. Because in markets, certainty is usually expensive. But clarity compounds. The BE Invested Labs platform is live now. You can generate AI-powered equity research reports, valuation analysis, and audio briefings on public companies in minutes.

Try the platform here:

And if you want more research notes like this, subscribe to BE Invested Labs.

— Buyce & Emmanuel

BE Invested Labs

Disclaimer

This article is for educational and research purposes only. It is not financial advice, investment advice, or a recommendation to buy or sell any security. Always do your own research and consider speaking with a licensed financial adviser before making investment decisions.

References And Data Notes

BE Invested Labs internal Sandisk Corporation institutional research report, generated June 3, 2026. The report initiated coverage with a Neutral rating, estimated fair value around $1,550 per share, and scenario values of $2,200 bull case, $1,500 base case, and $900 bear case.

Reuters reporting was used to cross-check Sandisk’s fiscal Q3 2026 revenue of $5.95 billion, adjusted EPS of $23.41, Q4 revenue guidance of $7.75 billion to $8.25 billion, and Q4 adjusted EPS guidance of $30 to $33. (Reuters)

Reuters reporting was also used to cross-check Sandisk’s long-term customer agreements, including five long-term agreements and three third-quarter agreements worth at least $42 billion, as well as the announced $6 billion share buyback. (Reuters)

Investor’s Business Daily and MarketWatch reporting were used to cross-check Q3 revenue, adjusted earnings, Q4 guidance, data centre strength, and market reaction after the earnings release. (MarketWatch)

Reuters and WSJ reporting were used to cross-check the January 2026 quarter, including Q2 revenue of $3.03 billion, adjusted EPS of $6.20, Q3 guidance at the time, and the extension of the Kioxia joint venture through 2034. (Reuters)

Reuters reporting was used to cross-check Western Digital’s partial sale of its Sandisk stake after the spin-off and the broader post-spin-off ownership context. (Reuters)

"Buy what you know" Peter Lynch.

Okay I'm not going to FOMO mode now.

Just annoyed when I completley overlook and even forget stocks of company that I personally use their product, shoot up without me ever investing in it 😂.

Definitely a good company, but currently I dont have confidence at this price due to the current AI ramp.