How To Get SpaceX Exposure Before The IPO: SMT vs ARK

Riding the rocket, or building one? A BE Invested Labs deep dive into Scottish Mortgage, ARK, and the danger of IPO FOMO.

If the internet has become a free university for investors, the tuition is your time. We built BE Invested so the tuition would be paid by AI.

Not because investors need more noise. Not because the world needs another finance dashboard filled with blinking red and green numbers. But because ordinary investors are constantly being pushed into the deep end of the market with too much information, too little structure, and very little help in turning all of that data into clear thinking.

Few things create more noise than a hyped IPO, especially when the company involved is SpaceX.

Recent reporting around a potential SpaceX IPO has created exactly the kind of environment where investors can become emotional: huge valuation expectations, limited public financials, index inclusion speculation, private-market mark-ups, and the quiet fear that everyone else might get rich before you. That fear has a name: FOMO. And FOMO is rarely a good investment strategy.

So the question is not simply, “How do I buy SpaceX?” The better question is: how do I think about SpaceX exposure without losing my discipline?

That is why, ahead of the launch of BE Invested Labs, we wanted to bring one of our research ideas into the public: Scottish Mortgage Investment Trust, ticker SMT.L. Scottish Mortgage is one of the most interesting publicly listed vehicles for investors who want exposure to SpaceX before it becomes fully public. But it is not a clean SpaceX investment. It is not risk-free. And it is definitely not something to buy blindly because the word “SpaceX” is attached to it.

This is not financial advice. It is a research framework. The goal is not to tell you what to buy. The goal is to show you how to think.

Why This Matters Right Now

SpaceX has become one of the most anticipated potential public listings in modern market history. Recent reporting has suggested that the company could target a valuation around $1.75 trillion, with some commentary pointing to even higher market expectations. If that happens, SpaceX would not be just another IPO. It would become one of the largest public market debuts ever attempted.

But the higher the excitement, the more disciplined investors need to become. SpaceX is not only a rocket company anymore. The investment story has expanded far beyond launches and reusable boosters. The broader SpaceX ecosystem now touches satellite internet through Starlink, artificial intelligence through xAI-related narratives, and potentially even the long-term idea of orbital infrastructure and AI compute.

That sounds exciting. It also sounds expensive. And that is the problem.

When a company is private, ordinary investors do not usually get the same access as institutions, venture funds, insiders, and early backers. By the time the public gets invited to the party, the early returns have often already been captured by someone else. That does not mean the IPO will fail. SpaceX may still become an extraordinary public company. But if the IPO arrives at a very high valuation, retail investors could be walking into a situation where the story is already priced for perfection.

That is why indirect routes matter. Not because they are perfect, but because sometimes the better question is not, “Can I buy the rocket?” Sometimes the better question is, “Can I own part of the launchpad?”

Meet Scottish Mortgage Investment Trust

Scottish Mortgage Investment Trust sounds like it should be a sleepy financial product from another era. It is not.

Despite the name, Scottish Mortgage is not a mortgage company. It is not simply a Scottish fund buying local businesses. It is a global investment trust managed by Baillie Gifford, with a long history of backing transformational growth companies. Founded in 1909, the trust is more than a century old, but its portfolio is anything but old-fashioned.

Its mandate is to invest in companies that management believes can shape the future of the global economy. That includes public companies, but also private companies that most ordinary investors cannot access directly. This is the key point. Scottish Mortgage gives public market investors a listed route into a portfolio that includes both public technology leaders and private innovation companies.

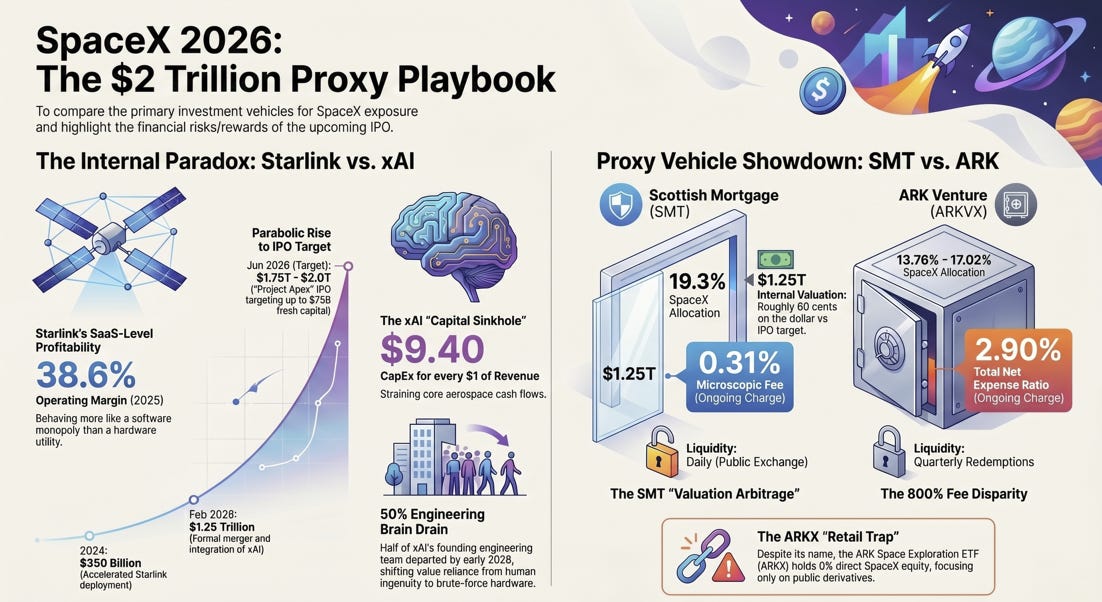

In that sense, SMT sits somewhere between a traditional global equity fund and a venture-style growth portfolio. That is why it matters in the SpaceX conversation. Scottish Mortgage owns a large stake in SpaceX, but it also owns much more than SpaceX. And that distinction is important.

Track Record At A Glance

Scottish Mortgage’s recent performance shows why it continues to attract long-term growth investors despite its volatility. Over the last year, SMT delivered a strong share price return and significantly outperformed the FTSE All-World Index over the same period. But the longer-term picture is more complicated. Over a five-year period, SMT’s annualised Net Asset Value return has lagged the FTSE All-World Index, reflecting the painful reset that growth and technology stocks experienced during the 2022 to 2024 interest-rate cycle.

That is the nature of this trust. When long-duration growth is loved, SMT can look brilliant. When long-duration growth is punished, SMT can look broken. Investors need to understand both sides before attaching themselves emotionally to the upside story.

What makes SMT different from a normal global index fund is its aggressive exposure to private innovation companies. A large portion of the trust is invested in private businesses such as SpaceX, ByteDance, Stripe, Databricks, and Anthropic. These are the kinds of companies that ordinary investors usually cannot access unless they are institutions, venture capital funds, or ultra-high-net-worth individuals.

The fee is also relatively low for what the trust offers. SMT’s ongoing charges are around 0.34%, which is modest considering the private market access, research depth, and active management involved. But low fees do not remove risk. They simply mean investors are not paying hedge-fund-style fees to access this strategy.

Management Philosophy

Scottish Mortgage is run by people with a very particular worldview. Tom Slater and Lawrence Burns are not trying to beat the market by trading around quarterly earnings. Their approach is built around patient ownership, long-term compounding, and the belief that a small number of exceptional companies can create most of the value in a portfolio.

This is the same philosophical world that allowed Baillie Gifford to back companies like Amazon and Tesla early and hold them through extreme volatility. That approach can be powerful, but it can also be uncomfortable. Long-term investing sounds beautiful when prices are rising, but it becomes emotionally difficult when a favourite holding falls sharply, the market turns against growth stocks, and everyone begins asking whether the managers have lost their touch.

That is the tension inside SMT. It is built for investors who can tolerate volatility in exchange for exposure to companies that may compound for a decade or longer. That is not everybody, and it should not be sold as if it is.

Top Holdings: Why SMT Is More Than A SpaceX Proxy

As of the latest data we reviewed, Scottish Mortgage’s largest holdings included a mixture of public and private companies across semiconductors, AI, digital platforms, payments, e-commerce, and space. The list includes names such as SpaceX, TSMC, NVIDIA, ASML, ByteDance, Amazon, Stripe, MercadoLibre, Meta, and Anthropic.

This matters because many investors will hear “SMT owns SpaceX” and immediately reduce the trust to a SpaceX proxy. That is too simplistic. SpaceX is a major part of the story, but SMT is not just a rocket bet. It is a portfolio built around the idea that the next era of global growth will come from companies building the infrastructure of the future.

That includes advanced chips, AI models, global e-commerce, digital payments, social platforms, cloud infrastructure, private space exploration, and next-generation software. In other words, SMT is not just asking whether SpaceX will win. It is asking whether the companies building the next technological layer of the economy will continue to compound.

That is a bigger thesis, and it deserves to be analysed that way.

How SMT Gets You Into SpaceX

Scottish Mortgage invested in SpaceX years before ordinary investors could even dream of buying the company on a public exchange. That early access is the entire point.

Most retail investors cannot buy SpaceX directly today. There are secondary market platforms and specialist products that may offer access, but they often come with restrictions, higher minimums, liquidity limits, accreditation requirements, or valuation uncertainty. SMT offers a simpler route. You buy the listed trust on the London Stock Exchange, and inside that trust is a stake in SpaceX.

But here is the important part: Scottish Mortgage does not value SpaceX based on hype headlines alone. Recent reporting shows Baillie Gifford has defended its SpaceX valuation using verifiable transaction data rather than media speculation. The trust has reportedly valued SpaceX around $1.25 trillion, even while some IPO speculation has pointed toward a much higher figure.

That matters because if SMT is valuing SpaceX more conservatively than the rumoured IPO price, there may still be upside if the public market eventually confirms a higher valuation. But there is also risk. If the IPO prices lower than expected, gets delayed, or trades poorly after listing, SMT shareholders could feel that too.

So SMT is not a magic trick. It is an access vehicle with benefits and trade-offs.

The NAV Question: Discount Or Premium?

One of the most important parts of understanding Scottish Mortgage is the relationship between its share price and its Net Asset Value. Net Asset Value, or NAV, is the estimated value of everything the trust owns after liabilities. If SMT’s share price is below its NAV, it trades at a discount. If its share price is above NAV, it trades at a premium.

Historically, Scottish Mortgage has often traded at a discount to NAV, especially when investors were worried about private company valuations, higher interest rates, or the broader growth stock sell-off. That discount was part of the attraction because it meant investors could sometimes buy a portfolio of high-growth public and private companies for less than the stated value of the underlying assets.

But this is where the analysis needs to be current. Recently, SpaceX-related optimism has helped push SMT back toward, and at times above, NAV. That changes the equation. Buying SMT at a discount is different from buying SMT at a premium. At a discount, you may be getting a margin of safety. At a premium, you are paying extra because the market is already excited.

So investors must not simply ask, “Does SMT own SpaceX?” They must also ask, “Am I paying a fair price for SMT today?” That is the type of question that separates investing from chasing.

The Fine Print

Owning SpaceX through SMT is not pure upside. Private company valuations are harder to assess than public market valuations. They are not priced every second like listed shares. They depend on funding rounds, secondary transactions, internal valuation work, and independent valuation processes. That means the reported value can move sharply when new information appears.

There is also concentration risk. SpaceX has become a very large part of SMT’s portfolio. That is exciting when SpaceX is being marked up, but it can become painful if sentiment changes. Then there is ByteDance exposure. ByteDance owns TikTok, and TikTok remains politically sensitive, especially in the United States. So SMT is not only taking technology risk. It is also taking regulatory and geopolitical risk.

Finally, there is the emotional risk. SMT can fall hard. Investors who cannot handle volatility should not pretend they are long-term growth investors just because the upside story sounds attractive. That is how people get shaken out at the worst time.

ARKX And Other Space Funds: The Comparison

When investors search for SpaceX exposure, ARK usually enters the conversation. That makes sense. Cathie Wood and ARK Invest are strongly associated with disruptive innovation, electric vehicles, space, robotics, AI, and high-growth technology. So naturally, many investors assume ARK must be the cleanest route to SpaceX exposure.

But the details matter. ARK Space Exploration & Innovation ETF, known as ARKX, sounds like the obvious SpaceX play. In reality, it does not own SpaceX directly. It is a space and aerospace-themed ETF that invests in listed companies connected to space exploration, defence, satellites, and enabling technologies. That includes companies such as Rocket Lab, L3Harris, Kratos, AMD, and others.

Those businesses may benefit from growth in the broader space economy. But owning ARKX is not the same as owning SpaceX. That distinction is crucial. ARKX owns the surrounding theme. SMT owns the private-market asset.

ARK Venture Fund is different. It does own private SpaceX shares, and therefore comes closer to the direct exposure many investors are looking for. But it also comes with different trade-offs: higher fees, different liquidity terms, a shorter track record, and venture-style valuation risk. Based on recent reporting, SpaceX has represented a mid-teens percentage of ARK Venture Fund at times, but that figure can change. Cathie Wood has also indicated ARK could rebalance its SpaceX position after the company becomes public.

So the key lesson is simple: do not buy a fund because the marketing theme sounds right. Look inside the vehicle. The name on the wrapper is not enough.

Other Public Vehicles With SpaceX Exposure

Scottish Mortgage is not the only listed vehicle with SpaceX exposure. Baillie Gifford US Growth Trust also provides access to SpaceX, although with a smaller weighting than SMT. It may appeal to investors who want Baillie Gifford’s growth philosophy but with more of a US-focused portfolio.

Schiehallion Fund, another Baillie Gifford vehicle, is also connected to later-stage private companies and has been discussed as part of the broader SpaceX exposure conversation. Other UK-listed vehicles and private market funds may also hold SpaceX stakes, but many of them either have smaller exposure, different mandates, less liquidity, or a portfolio that is not primarily focused on high-growth innovation.

So again, the question is not simply, “Which fund owns SpaceX?” The better question is: “How much SpaceX exposure am I really getting, what else am I buying, what fees am I paying, and what risks am I accepting?” That is the adult version of the conversation.

SMT vs ARK: The Practical Difference

When comparing the different ways to get exposure to SpaceX, the details matter more than the hype. Scottish Mortgage Investment Trust feels like the most balanced option because it gives investors a meaningful direct stake in SpaceX, but not in isolation. You also get exposure to other long-term growth companies across AI, semiconductors, fintech, and digital infrastructure, including names like ASML, NVIDIA, TSMC, Stripe, ByteDance, and MercadoLibre.

But let’s not romanticise it. SMT is volatile. A large portion of its assets are in private companies, which makes valuation less transparent. Its exposure to ByteDance brings China and regulatory risk. And as we saw during the growth stock correction, this trust can underperform badly when the market turns against long-duration technology businesses.

ARKX, on the other hand, sounds like a SpaceX play, but it does not actually own SpaceX. It gives exposure to the broader space and defence theme through companies like Rocket Lab, L3Harris, and Kratos. That may benefit from growth in the space economy, but it is not the same as owning SpaceX.

ARK Venture Fund comes closer because it does own private SpaceX shares, but the fees are higher, liquidity is more limited, and the exact SpaceX weighting can change over time. So the view is straightforward: if you want the cleanest “SpaceX only” exposure, none of these are perfect. But if you want meaningful SpaceX exposure inside a broader long-term innovation portfolio, SMT looks like one of the most practical options. Imperfect, yes. Volatile, definitely. But far more balanced than chasing IPO FOMO without understanding what you are paying for.

Beyond Rockets: The Semiconductor And AI Angle

One of the reasons SMT is interesting is that the SpaceX story is only one layer. The broader portfolio gives exposure to the companies building the infrastructure behind AI, semiconductors, cloud computing, digital platforms, and global commerce. This is where SMT becomes more than a SpaceX proxy.

NVIDIA and TSMC are central to the AI and semiconductor supply chain. NVIDIA provides the chips and computing platforms powering much of the AI revolution, while TSMC manufactures many of the world’s most advanced semiconductors. ASML is also critical. Without ASML’s lithography machines, the most advanced chips in the world become much harder to produce. That makes ASML less flashy than some AI companies, but structurally important.

Anthropic gives SMT exposure to private AI model development. Stripe gives exposure to digital payments infrastructure. MercadoLibre gives exposure to Latin American e-commerce and fintech. ByteDance and Meta represent different versions of the digital attention economy.

So when you buy SMT, you are not simply asking whether rockets will reach Mars. You are asking whether the next generation of economic infrastructure will be built by a concentrated group of exceptional technology companies. That is a very different thesis, and it is why SMT can be attractive even if someone is not obsessed with SpaceX.

The Human Element: Tom Slater, Lawrence Burns And Baillie Gifford

There is another thing that separates Scottish Mortgage from an ETF: it is actively managed. That means you are not just buying a basket of stocks. You are buying the judgement of Baillie Gifford’s investment team.

Tom Slater has been closely associated with Scottish Mortgage’s long-term growth approach. Lawrence Burns also plays a key role in the trust’s management. Together, they represent a philosophy that is very different from short-term market timing. They are looking for outliers, the kind of companies where one or two winners can drive a large part of the portfolio’s long-term return.

That approach requires patience. It also requires a willingness to look wrong for long periods of time. And that is where investors need self-awareness. It is easy to say you believe in long-term investing when the chart is going up. It is much harder when the market disagrees with you for two years and the comment section starts calling your favourite fund a disaster.

SMT’s approach can produce extraordinary returns when it works. But it can also produce painful drawdowns. That is the bargain. You do not get venture-style upside without venture-style discomfort.

How We Would Frame The Decision

This is not financial advice. This is the framework we would use.

First, define your objective. Do you want pure SpaceX exposure, or do you want a diversified innovation portfolio with SpaceX as a major growth engine? If you want pure SpaceX exposure, SMT is not perfect because it owns many other companies. But if you want meaningful SpaceX exposure plus AI, semiconductors, digital platforms, fintech, and private market optionality, SMT becomes much more interesting.

Second, check the price you are paying. Is SMT trading at a discount or a premium to NAV? This matters because a great portfolio can become a poor investment if bought at the wrong price.

Third, understand the private market risk. Private holdings can be powerful, but they are less transparent. They can be marked up, but they can also be marked down. Fourth, compare fees and liquidity. ARKX gives daily ETF liquidity but no direct SpaceX ownership. ARK Venture Fund gives direct private-market exposure but with higher fees and less straightforward liquidity. SMT sits somewhere in the middle: listed, liquid, lower fee, but still exposed to private company valuation risk.

Finally, be honest about your temperament. If you cannot handle volatility, SMT may not be for you. If you buy because of SpaceX excitement and panic when the trust falls 25%, the problem is not the trust. The problem is the mismatch between the investment and your psychology.

Our View

At BE Invested Labs, we see SMT as one of the most pragmatic publicly listed ways for everyday investors to gain meaningful SpaceX exposure while also participating in other long-term growth themes such as AI, semiconductors, fintech, and digital infrastructure.

That does not mean SMT is a “buy at any price.” It is not. It means SMT deserves serious research because it gives ordinary investors access to a type of portfolio that would otherwise be difficult to build.

ARKX gives you the space theme, but not direct SpaceX ownership. ARK Venture Fund gives you private SpaceX exposure, but with higher costs, different liquidity terms, and changing weightings. SMT gives you a large SpaceX stake inside a wider innovation portfolio, managed by a team with a long-term growth philosophy.

That is why it stands out. But the key word is “framework.” Do not buy stories. Analyse structures. Because a good story does not retire you. Productive assets do.

What Happens Next — And Where BE Invested Comes In

We built BE Invested Labs because we kept seeing the same pattern. A friend would ask about the next hot stock. Someone would send a video about an IPO. A headline would go viral. Then suddenly everyone would be opening ten tabs, reading conflicting opinions, checking Reddit, watching YouTube, and still ending up more confused than when they started.

That is not research. That is modern financial noise.

Our platform is designed to turn that noise into structured analysis. With BE Invested Labs, users will be able to generate research reports on public companies, run valuation models, compare scenarios, save reports in a research library, and listen to AI-generated audio briefings.

The idea is simple: less scattered research, more structured thinking.

Ahead of our launch, this article is an example of the kind of work we want to bring to ordinary investors. Not hype. Not predictions dressed up as certainty. But structured analysis that helps you think better.

Our waitlist is open now:

If you want early access, join the list. Our first users will help shape the product directly.

Closing Thoughts

We are living through a period where innovation moves faster than regulation, narratives move faster than earnings, and retail investors are often asked to make decisions with incomplete information. That is dangerous, because in markets, the loudest story is not always the best investment.

SpaceX may become one of the greatest public companies of the next decade. Or it may list at a valuation that already assumes too much perfection. We do not know yet. But we do know this: chasing hype is not a strategy. Research is.

By looking at SMT, ARKX, ARK Venture Fund, and other possible routes, we are not trying to crown one perfect winner. We are trying to understand the structure behind the exposure. Because the goal is not to be first into the hottest IPO. The goal is to build wealth with clarity.

And clarity compounds.

See you on launch day.

— Buyce & Emmanuel

BE Invested Labs

And if you want early access to the platform behind this analysis, join the waitlist before launch: BE Invested Waitlist

Disclaimer

This article is for educational and research purposes only. It is not financial advice, investment advice, or a recommendation to buy or sell any security. Always do your own research and consider speaking with a licensed financial adviser before making investment decisions.

References And Data Notes

Scottish Mortgage Investment Trust official factsheets, annual reports, and manager commentary were used for portfolio holdings, ongoing charges, private company exposure, performance data, and management information.

Reuters reporting was used for SpaceX IPO timing, potential valuation expectations, and possible fast index inclusion following new FTSE Russell rules. (Reuters)

The Times reporting was used for Scottish Mortgage’s SpaceX holding, portfolio weighting, Tom Slater’s commentary, share buyback activity, and recent investor optimism around the trust. (The Times)

BE Invested Labs internal SMT.L research report and the uploaded draft were used as the base research file for this article.

| A guest post by

|