Business Breakdown: Pagaya Technologies, the AI Credit Network Still Waiting for Its Cycle Test

Pagaya is profitable, cash generative, and trading at low multiples. The question is whether its AI credit network can hold through a tougher consumer credit cycle.

Pagaya Technologies is one of the more debated small-cap fintech names in the market.

The bull case sounds simple at first: the company is profitable, growing, using AI to improve credit decisions, and trading at a low valuation compared with many fintech peers.

The bear case is just as direct: Pagaya still depends on consumer credit, securitization markets, institutional funding, partner concentration, and risk-retention assets.

Both sides have evidence.

That is why this business is worth breaking down properly.

This article was also written as a response to Deacon Brantley’s Flashpoint article, “The Next Visa: A Deep Dive Into Pagaya.” Deacon made a strong argument that the market may be treating Pagaya like a risky lender when the business is closer to a fee-based credit network.

We agree with part of that framing.

We also think the Visa comparison needs limits.

Pagaya may be a credit network. It is also a credit network operating inside consumer lending and asset-backed securitization markets.

That distinction matters.

The 30-second view

Pagaya is an AI-powered credit platform.

It works with banks, fintech lenders, auto finance providers, and point-of-sale financing partners. When a borrower fails a lender’s first credit screen, Pagaya can take a second look using its AI model.

If Pagaya’s system sees an acceptable risk-return profile, the borrower may still receive an offer. The lending partner keeps the customer relationship. Institutional investors fund the exposure, often through asset-backed securitizations. Pagaya earns fees from the transaction flow.

The opportunity is clear. Pagaya may be building a capital-light credit network that sits between lenders and institutional capital.

The risk is also clear. The model depends on credit performance, funding markets, partner flow, and investor appetite for consumer credit.

Our current view is constructive, but strict.

Pagaya is improving fast enough to deserve a serious re-rating discussion. The company still needs a credit-cycle discount until FRLPC, partner concentration, retained-risk exposure, and ABS funding prove durable under stress.

If you want more stock breakdowns like this, subscribe to BE Invested Labs.

What Pagaya actually does

Pagaya sits inside the consumer credit process.

A borrower applies for a loan or financing product through a lending partner. The partner uses its own underwriting model first. If the borrower does not pass that model, Pagaya can evaluate the application again.

That second look is the business.

Pagaya uses machine learning, repayment data, and its credit models to decide whether the borrower can be approved at an acceptable risk level. If the answer is yes, the loan can be originated by the partner and funded through Pagaya’s capital network.

Pagaya connects 3 sides:

Lending partners that want more approved customers.

Borrowers who may be rejected by traditional models.

Institutional investors looking for consumer credit assets.

The company makes money when credit flows through that network.

That structure is attractive because Pagaya does not need to spend like a consumer app to acquire borrowers directly. It plugs into partners that already have customer demand.

That is the B2B2C logic.

Pagaya gets access to demand through its partners. Partners get more approvals without taking the full balance-sheet risk. Institutional investors get access to credit assets.

When this works, Pagaya can look like a platform. When funding markets tighten, it can look much closer to a credit-cycle business.

Why the market may be misreading PGY

Pagaya still carries SPAC-era baggage.

That matters. Many investors got burned by growth fintech names that promised a lot, lost money, and then got hit by higher interest rates.

Pagaya was part of that broader group. The market does not easily forget.

The company is now trying to prove that the old version of the story is outdated.

The numbers have improved. Pagaya reported its fifth consecutive quarter of GAAP profitability in Q1 2026. It also raised full-year 2026 net income guidance.

That changes the discussion. The question is no longer whether Pagaya can produce any profit at all. The question is whether the profit is durable enough to deserve a higher multiple.

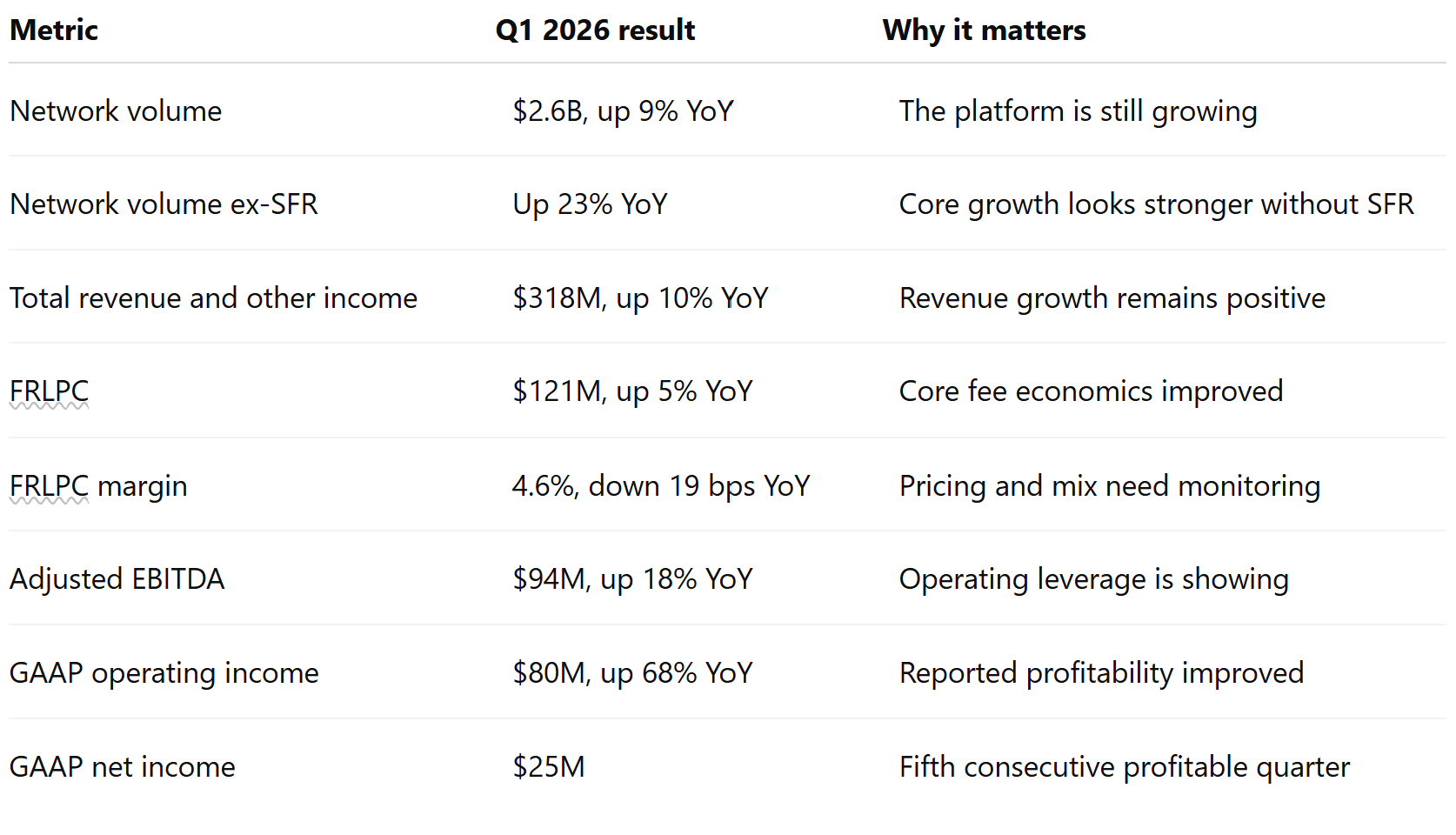

Q1 2026 scorecard

Pagaya’s Q1 2026 report was strong on the surface.

The clean positive signal is profit growth.

Revenue grew 10%. Adjusted EBITDA grew 18%. Operating income grew 68%. That means revenue is growing faster than some major cost lines. For a platform-style business, that is exactly what investors want to see.

The more cautious signal is FRLPC margin.

FRLPC increased 5%, but FRLPC as a percentage of network volume fell to 4.6%. Pagaya said this reflected asset class mix, new partner contributions, tighter ABS pricing, higher cost of capital, and market conditions.

That is important. If volume grows but Pagaya earns less per dollar of volume, the quality of growth can weaken. If FRLPC stabilises while volume grows, the thesis gets cleaner. For Pagaya, FRLPC is one of the most important numbers to track.

If you know someone watching PGY, fintech, AI lending, or consumer credit, share this breakdown with them.

The number management wants investors to notice

Management highlighted that network volume grew 23% excluding SFR.

That is useful. It tells us that the core business looks stronger when Single-Family Rental is removed from the comparison.

It also needs context.

Headline network volume grew 9%. Ex-SFR growth was 23%. That gap tells us SFR affected the comparison and should not be ignored.

Our BE Invested Labs earnings-call sentiment report flagged this as a narrative shift. In earlier periods, SFR had been part of the broader diversification story. In Q1 2026, the main narrative focused more on Auto and Point-of-Sale growth, while SFR moved into the background.

That does not mean management is hiding a disaster.

It means investors should separate headline growth, ex-SFR growth, and the quality of growth by vertical.

The best version of the bull case does not need SFR to be ignored. It needs personal loans, auto, and POS to grow with healthy economics.

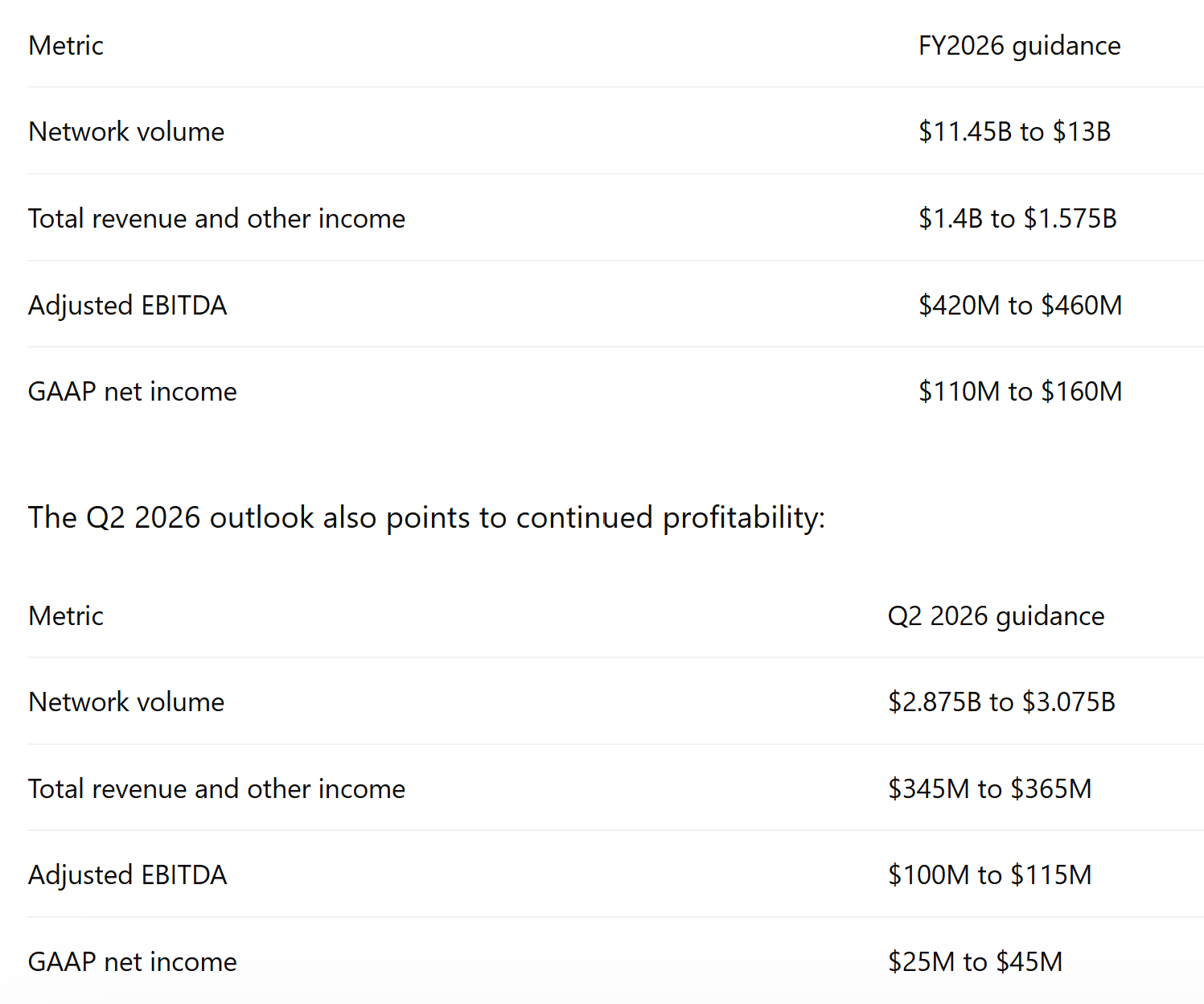

Guidance is stronger, but the test is still ahead

Pagaya raised its full-year 2026 outlook.

This is a meaningful step.

Pagaya is guiding for full-year GAAP net income, not only adjusted EBITDA.

That matters because the market has been skeptical of many fintech companies that rely heavily on adjusted metrics.

Still, guidance is not proof of durability.

Management can control costs and risk posture. It cannot fully control unemployment, interest rates, ABS spreads, securitization demand, or consumer credit stress.

The next few quarters should be judged by quality:

Is growth broad across products?

Is FRLPC stable?

Are ABS deals clearing at workable spreads?

Are credit losses within expectation?

Are retained interests holding their value?

Is GAAP net income still growing without too much dependence on adjustments?

Those are the questions that matter.

Why the Visa comparison works

Deacon’s Visa framing is useful because it forces investors to think about category.

Visa does not lend money to cardholders. It connects banks, merchants, and cardholders, then earns fees across the network.

Pagaya wants a similar position in credit origination.

It wants to sit between lenders and institutional capital. It wants to approve more borrowers, route exposure to funding partners, and earn fees from the flow.

That is a good business if it works.

The model has the ingredients investors usually like:

Low direct customer acquisition cost.

Partner distribution.

Data accumulation.

Fee-based revenue.

Operating leverage.

More volume flowing through one infrastructure layer.

That is why PGY can look mispriced.

If the market treats Pagaya like a distressed lender, the valuation can stay low. If the market starts treating Pagaya as a profitable credit network, the multiple can expand.

That is the bull case in one sentence.

Where the Visa comparison breaks

Visa does not depend on securitizing consumer loans.

Pagaya does.

That is the main difference.

Pagaya’s business still depends on institutional investors wanting consumer credit exposure. It also depends on securitization markets staying open at acceptable economics.

If ABS investors pull back, Pagaya’s network gets harder to run.

If consumer defaults rise, retained assets can be marked down.

If funding spreads widen, FRLPC can compress.

If a large partner reduces volume, the network effect can look weaker than expected.

This is why PGY should not be analysed with one label.

The business is not a traditional lender. It is also not Visa.

A better category is this:

Pagaya is an AI credit network whose value depends on underwriting quality, funding access, partner depth, and credit-cycle durability.

That is the more precise thesis.

Cash conversion is the strongest pushback against the bear case

One of the best points in Pagaya’s favour is cash conversion.

Our BE Invested Labs forensic accounting report found that in FY2025 Pagaya generated $238.6M of operating cash flow against $81.4M of GAAP net income.

That is about $2.93 of operating cash flow for every $1 of reported earnings.

That matters.

A common bear argument is that Pagaya’s profitability may be heavily shaped by accounting marks, fair value adjustments, securitization structures, or retained interests.

Cash flow does not answer every question, but it makes the “accounting profit only” argument harder.

The business is producing cash.

The caution is that Pagaya also uses cash and capital to support risk-retention assets and securitization-linked investments. So cash conversion should be read alongside the balance sheet, not in isolation.

The clean view:

Cash generation has improved. The balance sheet still needs careful reading.

The Buffett test: yellow, not green

Our Warren Buffett-style financial statement report gave Pagaya a yellow-light verdict across balance sheet, earnings quality, and cash generation.

That is the right tone.

Pagaya is improving, but it is not yet the clean, predictable compounder that a strict Buffett-style investor would call obvious.

The positives are clear:

Revenue has scaled.

GAAP profitability has returned.

Cash generation improved.

Gross margins have recovered above 40%.

The model is less asset-heavy than a traditional lender.

The concerns are also real:

Cash flow has been volatile historically.

Owner earnings only recently turned positive.

Debt and retained-risk exposure matter.

Dilution remains a factor.

The balance sheet is not a true fortress yet.

The model has not been fully proven through a severe consumer downturn.

This does not kill the thesis.

It defines the margin of safety problem.

Pagaya may be cheap. It is not simple.

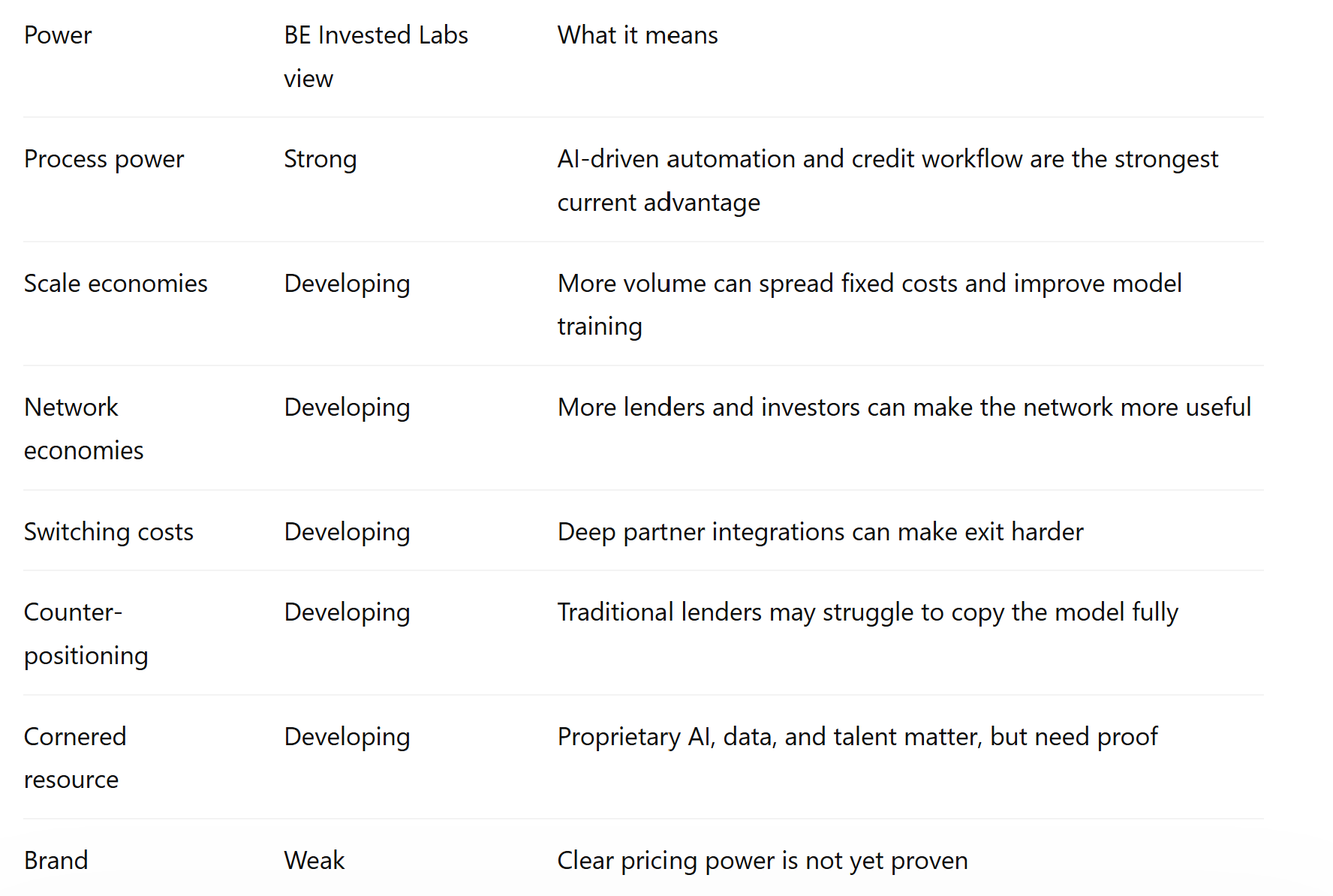

The moat: process power first

Our 7 Powers report is useful here because it avoids overclaiming.

Pagaya’s strongest power today is process power.

The company has built an AI-driven process for evaluating credit, connecting partner flow with institutional capital, and scaling decisions through technology. If the model keeps improving with more data, that process can become harder to replicate.

Other powers are still developing:

This is a better view than simply saying Pagaya has a strong moat.

The moat is real enough to study.

It is not proven enough to take for granted.

The key issue is credit stress. A credit moat needs to survive bad vintages, not only strong quarters.

Partner concentration is still real

Pagaya often talks about its broad partner network.

That is fair. The company says it has more than 30 lending partners and has evaluated more than $3.7T in applications since inception.

The risk is concentration.

Our BE Invested Labs business model report flagged that the top 5 lending partners accounted for about 61% of total network volume in Q1 2025. It also flagged that the top 5 ABS funding partners accounted for 47.5% of total ABS funding.

Those numbers matter.

A company can have many partners and still depend heavily on a few.

This is one of the most important risks to watch. If the top few lending partners reduce volume, change strategy, renegotiate economics, or build more internally, Pagaya’s growth can slow quickly.

The same applies to funding partners.

If a few major ABS investors pull back, the funding side of the platform can become more expensive or less reliable.

The bull case needs more evidence of broader volume contribution over time.

Funding execution is improving

Pagaya has been active in ABS markets.

In Q1 2026, the company raised $2.1B of ABS funding across 4 transactions despite market volatility. It also received its first AAA Fitch rating on a $368M PAID resecuritization.

After Q1, Pagaya closed RPM 2026-3, a $600M upsized auto ABS transaction. The company said it was its largest auto ABS deal to date and its third fully pre-funded auto ABS transaction of 2026. Pagaya also said it had raised $1.5B of pre-funded auto ABS in 2026 and more than $38B across 90 ABS transactions since 2018.

That supports the bull case.

Funding demand is not theoretical. Pagaya continues to raise capital through its structures.

The risk is that funding quality can change before volume does.

ABS access should be watched through 3 lenses:

Can Pagaya keep issuing deals?

At what spread and structure?

How much risk does Pagaya need to retain to get deals done?

The first answer is currently positive. The second and third will decide how attractive the model remains.

Product expansion: Upgrade Flex Pay matters

Pagaya also announced an expansion of its partnership with Upgrade into Flex Pay, Upgrade’s BNPL product.

This is relevant because it supports the diversification thesis.

Pagaya has been trying to expand beyond personal loans into auto and point-of-sale financing. The Upgrade Flex Pay announcement gives another proof point that Pagaya’s partner relationships can move into new products.

That matters because one-product dependence would make the business more fragile.

The caution is that new verticals can carry different economics. Growth in a new asset class is useful only if underwriting quality, funding demand, and FRLPC economics hold.

For now, the Upgrade expansion is a positive signal. It does not settle the full thesis.

Management tone: confident, but careful

The Q1 management message was confident.

The company is pointing to 5 consecutive quarters of GAAP profitability, operating leverage, product expansion, and stronger funding execution.

That is the right message to give after years of investor skepticism.

Our earnings-call sentiment report still found caution underneath the confidence.

Management is talking about tighter risk controls, higher borrower income profiles, higher cost of capital, and tighter ABS pricing. Those comments matter because they show the company is adapting to a tougher credit environment rather than ignoring it.

That is good risk management.

It also confirms that the environment is not easy.

The CFO transition is worth watching too. Evangelos Perros is stepping down as CFO and Jon Dobres is taking over, while Perros remains as a strategic executive adviser through the end of 2026.

A CFO transition is not automatically a red flag.

But after a period of improving profitability, investors should watch whether reporting discipline, guidance quality, and capital allocation remain consistent.

The Upstart comparison

The hardest question for Pagaya is Upstart.

Upstart also had an AI credit story. It also promised better underwriting. It also looked powerful when capital was available and loan demand was strong.

Then the cycle changed.

Funding pressure, credit concerns, and macro uncertainty damaged the thesis.

Pagaya has differences that matter.

Its partner base appears broader. Its asset mix includes personal loans, auto, and point-of-sale financing. It has active securitization programs. It has reported 5 consecutive quarters of GAAP profitability. It has shown stronger cash conversion recently.

Those differences are meaningful.

The shared risk is still credit.

AI underwriting gets judged during stress. A model can look strong when borrowers are employed, capital markets are open, and losses are manageable. The real test comes when unemployment rises, funding spreads widen, and institutional buyers become more selective.

Pagaya has not yet proven the model through a full-scale consumer credit downturn as a mature public company.

That is the open question.

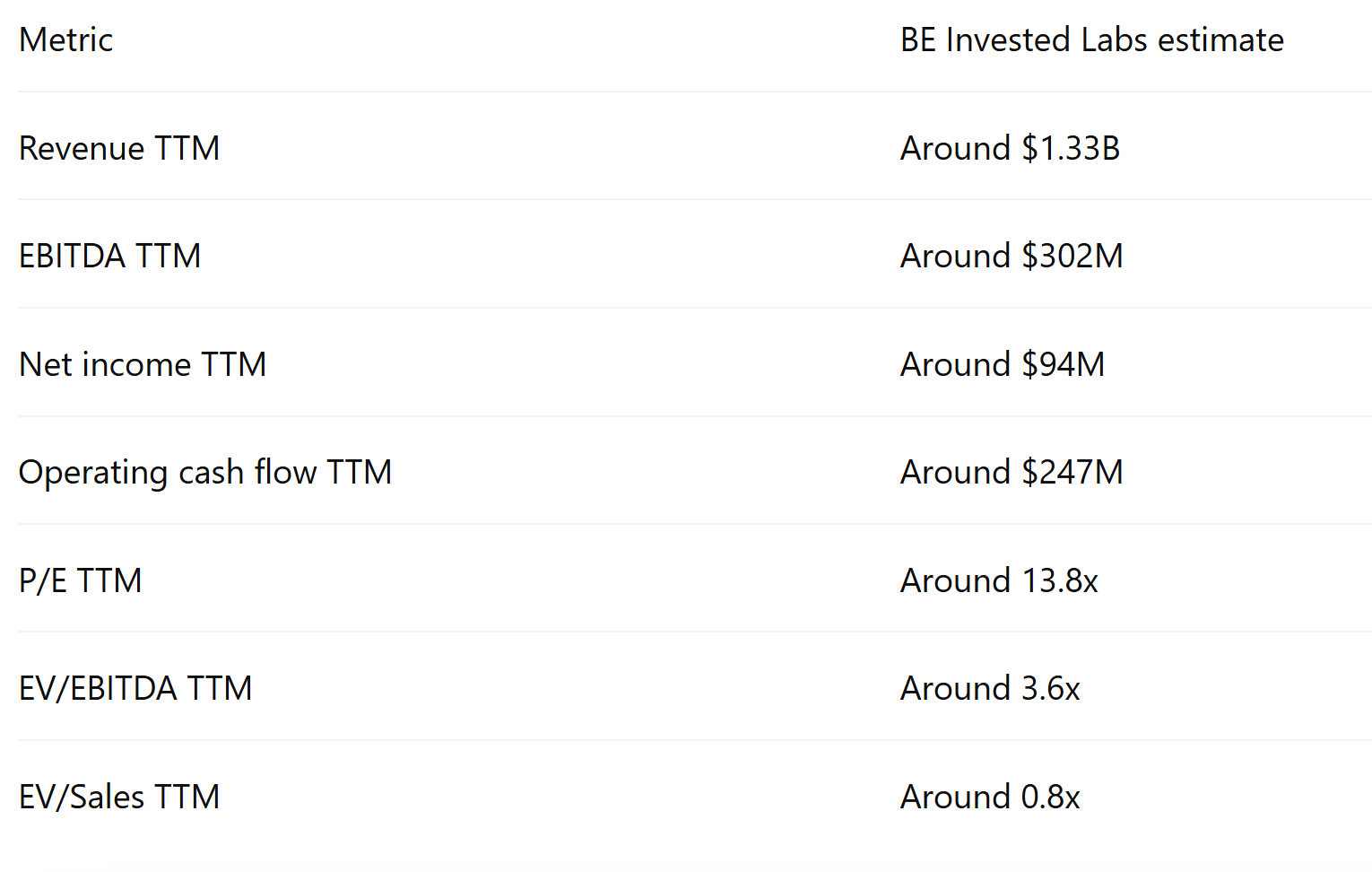

Valuation: cheap for a reason, still worth studying

At the latest price we checked, PGY traded around $15.42.

Our BE Invested Labs reports used a similar reference price and showed the following valuation picture:

Those are not demanding multiples if Pagaya keeps growing profitably.

Our neutral BE Invested Labs synthesis estimated fair value around $22.50 per share using a blend of DCF and peer-relative valuation. That was not a price target promise. It was a framework.

A bullish scenario can produce much higher values if the market starts treating Pagaya as a scalable credit network.

A bearish scenario can still take the stock lower if credit losses rise, ABS markets tighten, FRLPC compresses, or retained interests get marked down.

The valuation is attractive enough to study.

The risk is large enough to demand discipline.

The bull case

The bull case rests on 6 points.

1. The market may be using the wrong category

If Pagaya is treated as a distressed lender, the low multiple makes sense. If it earns trust as a profitable credit network, the multiple can expand.

2. GAAP profitability is now visible

Pagaya has reported 5 consecutive quarters of GAAP profitability. Management guided FY2026 GAAP net income of $110M to $160M.

That moves the discussion from promise to execution.

3. Operating leverage is showing

Revenue grew 10% in Q1 2026. Adjusted EBITDA grew 18%. Operating income grew 68%.

That is a strong profit conversion signal.

4. Cash conversion supports earnings quality

FY2025 operating cash flow was much higher than GAAP net income in our forensic report. That supports the idea that recent profitability is not only accounting presentation.

5. Funding execution remains active

Pagaya continues to issue ABS deals, including the $600M upsized auto ABS transaction after Q1.

Funding access is not theoretical.

6. Product expansion is real

Auto and POS are becoming more central to the story. The Upgrade Flex Pay expansion supports the idea that Pagaya can grow beyond one product line.

The bear case

The bear case also has 6 points.

1. Credit markets still drive the model

Pagaya depends on consumer credit performance and institutional demand for credit assets. A weaker credit cycle can pressure both sides.

2. FRLPC can compress

Q1 FRLPC margin fell to 4.6%. The decline was not dramatic, but the direction matters. If the company grows volume at weaker unit economics, the quality of growth changes.

3. Partner concentration is high

The top 5 lending partners represented about 61% of network volume in Q1 2025, according to our business-model report. That limits how far investors should push the diversification argument.

4. Funding concentration matters too

The top 5 ABS funding partners represented 47.5% of ABS funding in the same report. A broad funding network is useful, but large funding partners still matter.

5. AI underwriting is hard to verify externally

Investors can see outcomes. They cannot fully inspect the model. One weak vintage can damage trust quickly.

6. Regulation can change the economics

AI in lending faces scrutiny around fairness, bias, explainability, consumer protection, and data privacy. Regulation could increase compliance costs or limit how models are used.

What could break the moat

The moat breaks if the process stops producing better outcomes.

That can happen in several ways.

AI underwriting becomes easier to copy. Competitors catch up. Traditional lenders build more internally. Data access becomes restricted. Regulation limits model flexibility. Partner churn rises. ABS investors demand much higher yields. Credit performance deteriorates.

The most damaging version would be a credit downturn that exposes poor underwriting and weakens investor confidence at the same time.

That would attack both sides of Pagaya’s network.

Lenders would send less flow or demand better terms. Investors would demand more yield or reduce funding. Pagaya would face lower volume, lower FRLPC, and weaker retained-interest values.

That is the real bear case.

What we would watch next

For us, the next 4 quarters matter more than the story.

Here is the BE Invested Labs watchlist:

This is the work investors need to do.

Not deciding whether PGY is “the next Visa” or “the next Upstart.”

The work is tracking whether the numbers confirm the category the market is being asked to accept.

How we would frame Pagaya today

Pagaya is a profitable AI credit network with improving operating metrics, active ABS funding, and a valuation that may be too low if the business keeps executing.

It is also tied to consumer credit, capital markets, partner concentration, and retained-risk exposure.

That combination creates both the opportunity and the danger.

Deacon is right to challenge the lazy version of the market view. Pagaya is no longer just another SPAC-era fintech promising future profits. The company is producing GAAP net income, raising guidance, issuing ABS deals, and expanding product relationships.

The stricter view is that the final test has not arrived.

A tougher credit cycle will show whether Pagaya’s underwriting, funding network, partner relationships, and retained-risk structure deserve a higher multiple.

Until then, PGY sits in a difficult but useful category:

A business that may be better than its market reputation, but still needs to prove that its model works when conditions get worse.

Try the research process yourself

Pagaya is exactly the kind of company we built BE Invested Labs to analyse.

The story is attractive. The numbers are improving. The risks are real. The accounting is not simple. The valuation depends heavily on assumptions.

That is where structured research matters.

You can test the platform with PGY or another company you already follow:

Run the stock through the research flow. Compare the bull case and bear case. Check the valuation assumptions. Look at the financials. Ask whether the thesis still makes sense after the risks are visible.

That is the point of BE Invested Labs: Clearer research before stronger conviction.

Final view

Pagaya deserves serious attention.

The company is profitable, cash generative, and growing in areas that matter. It has active funding access, improving operating margins, and a business model that could be worth more than the market currently gives it credit for.

The risk side is just as important. Pagaya still depends on ABS markets, consumer credit health, partner flow, funding demand, retained-risk performance, and management discipline.

Our view is constructive, but strict.

PGY becomes more compelling if 4 things happen:

GAAP profitability continues.

FRLPC margin stabilises.

Partner and funding concentration improve.

ABS execution remains healthy through tougher conditions.

If those hold, the market may need to rethink Pagaya. If they break, the discount may be justified.

That is the thesis.

Pagaya is not a simple AI story. It is a test of whether AI underwriting, partner distribution, and institutional funding can create a durable credit network through a full cycle. That test is still open.

Reader question

What would you focus on first with Pagaya?

Valuation

Credit risk

ABS funding

Partner concentration

AI underwriting quality

FRLPC margin

Drop your answer in the comments. We may use the strongest questions for a follow-up breakdown.

Sources used

Pagaya Q1 2026 earnings release and shareholder materials.

Pagaya 2025 annual report and risk disclosures.

Pagaya May 2026 auto ABS announcement.

Pagaya June 2026 Upgrade Flex Pay partnership announcement.

BE Invested Labs PGY research reports: business model, earnings-call sentiment, forensic accounting, moat analysis, Buffett-style financial statement review, and valuation synthesis.

Flashpoint by Deacon Brantley: “The Next Visa: A Deep Dive Into Pagaya.”

Disclaimers & Disclosures

AI Transparency: B.E Invested Labs uses AI to aggregate financial data and format reports. The AI structures the information. Users determine their own investment thesis, risk management, and market outlook. We audit the system outputs to reduce AI errors. We use these exact reports to manage our own capital.

Legal Disclaimer: This platform provides educational and informational content. B.E Invested Labs is not a registered investment advisor and does not provide financial, investment, tax, or legal advice.