Business Breakdown: Brookfield Corporation, the real-asset allocator

How Brookfield built one of the most complex capital allocation businesses in the world. Disclaimer, we do have positions in Brookfield Corporation.

Brookfield is easy to respect and hard to understand.

At first glance, it looks like a holding company. Then you realize it owns pieces of an asset manager, an insurance business, infrastructure platforms, renewable power assets, real estate, private equity businesses, credit strategies, and listed partnerships.

After that, the picture becomes clearer. Brookfield raises long-term capital, buys real assets, improves them, sells mature assets, and reinvests the proceeds.

That is the Brookfield model.

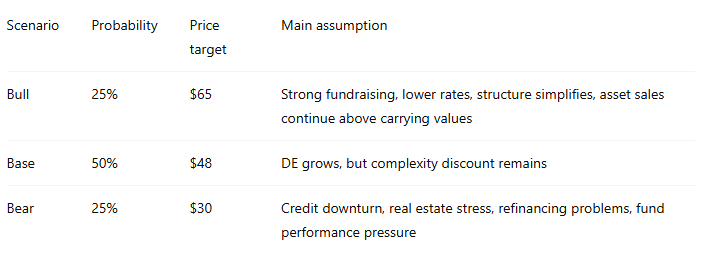

The BE Invested Labs research platform rates Brookfield Corporation (BN) as Neutral, with a probability-weighted fair value estimate of $48 per share. The bull case is $65. The bear case is $30. At the report price of $45.03, the implied upside to fair value was around 6.6%.

That matters because Brookfield is not a weak business. It is one of the most respected real-asset investment firms in the world.

The rating is Neutral because quality and complexity are both high. The business is impressive. The valuation gives less margin of safety than we would want for a company with this much debt, internal capital movement, non-IFRS reporting, and exposure to credit markets.

The useful question is simple:

Can Bruce Flatt and the Brookfield team keep investing larger amounts of capital at strong returns without the structure becoming too complex for public investors to properly value?

Our answer: probably yes over the long term, but the current setup still requires trust, patience, and valuation discipline.

We generated an audio briefing from the BE Invested Labs Brookfield research report. It walks through the company’s structure, moat, valuation, bull case, bear case, and the main risks in a podcast-style format.

The short version

Brookfield Corporation is a global investment firm focused on real assets and alternative investments.

It makes money from 5 main sources:

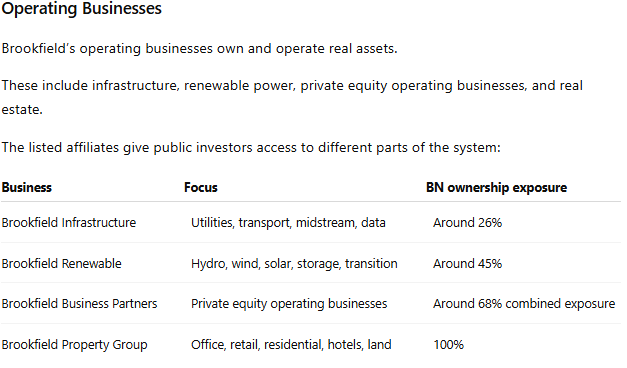

Management fees from Brookfield Asset Management.Performance fees and carried interest when funds perform well.Investment returns from capital Brookfield invests alongside clients.Insurance spread from Brookfield Wealth Solutions.Distributions and asset sales from operating businesses. The structure looks complicated because it is complicated. Brookfield Corporation owns roughly 73% of Brookfield Asset Management, owns and controls Brookfield Wealth Solutions, owns large stakes in Brookfield Infrastructure, Brookfield Renewable, Brookfield Business Partners, and owns Brookfield Property Group.

The center of the thesis is Brookfield Asset Management.

BAM raises money from pension funds, sovereign wealth funds, insurance companies, endowments, wealthy individuals, and private wealth channels. BAM invests that money into infrastructure, renewable power and transition, real estate, private equity, credit, and other private-market strategies. BAM charges fees on the capital and earns carried interest if fund returns pass the required hurdles.

Brookfield Corporation then benefits in 3 ways: it owns most of BAM, invests its own capital into BAM strategies, and uses BAM’s platform to invest insurance and operating business capital.

This is the strength of Brookfield. It is also the risk.

If BAM keeps producing strong returns, the whole Brookfield system can keep compounding. If BAM stumbles, the weakness spreads across fees, insurance returns, carried interest, reputation, and BN’s own investment returns.

The story: from Brazil to global alternatives

Brookfield’s history starts long before most modern asset managers existed.

The company traces its roots to 1899, when São Paulo Tramway, Light and Power Company was incorporated. The original business helped build electricity and tram infrastructure in Brazil. Over time, the company became Brazilian Traction, then Brazilian Light and Power, then Brascan.

The name Brascan came from Brazil and Canada.

The company slowly moved from operating utilities in Brazil to owning and managing real assets across different markets. In 1997, Brascan merged with The Edper Group to form EdperBrascan. In 2000, the company changed its name back to Brascan Corporation. In 2005, it became Brookfield Asset Management.

The Bruce Flatt era began in 2002, when he became CEO.

That period changed the scale of the company. Brookfield moved deeper into infrastructure, renewable power, real estate, credit, distressed assets, and private equity. It built listed vehicles for retail and institutional investors. It bought and sold assets across cycles. It became one of the largest alternative asset managers in the world.

Then came the 2022 split.

Brookfield Asset Management Inc. changed its name to Brookfield Corporation, ticker BN. The asset management business was separated into a new publicly listed Brookfield Asset Management, ticker BAM. BN kept a large ownership stake in BAM and continued to own its operating businesses and wealth solutions platform.

This is why BN and BAM should not be treated as the same company.

BAM is the asset manager. BN is the parent investment company that owns BAM shares, operating assets, insurance exposure, and invested capital across the Brookfield group.

That distinction matters for valuation.

BAM is cleaner. BN is more complex. BAM earns fees. BN gets fees indirectly, investment returns, insurance earnings, operating business distributions, carried interest, and asset sale gains.

BN has more ways to win. It also gives investors more moving parts to understand.

How Brookfield is structured

Brookfield Corporation has 3 main parts.

Asset Management

This is Brookfield Asset Management.

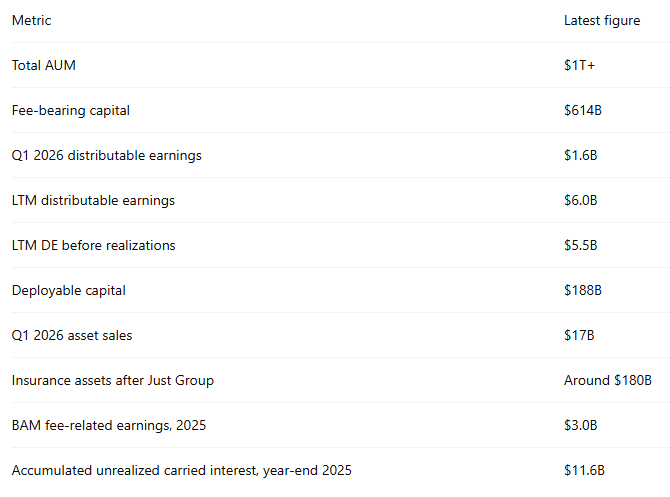

BAM manages more than $1 trillion of assets across infrastructure, renewable power and transition, private equity, real estate, and credit. It earns management fees on fee-bearing capital and can earn carried interest when funds deliver strong returns.

This is the highest-quality part of Brookfield’s structure because fee-related earnings are recurring, high-margin, and linked to capital that is often locked up for long periods.

For BN, the asset management business matters in 4 ways:

BN owns around 73% of BAM.

BN receives value as BAM’s fee-related earnings grow.

BN can earn carried interest through BAM’s fund performance.

BN invests its own capital into and alongside BAM-managed funds.

At year-end 2025, Brookfield valued its stake in the Asset Management business at $61.5B. BAM generated $3.0B of fee-related earnings, up 22% year over year. Brookfield also had $11.6B of accumulated unrealized carried interest before direct costs, with $9.4B attributable to the Corporation.

That is one of the big valuation arguments.

If BAM keeps growing fee-bearing capital and turns unrealized carry into realized cash over time, BN’s value should rise.

Wealth Solutions

This is Brookfield’s insurance business.

The simple version: Brookfield takes in long-duration insurance and retirement liabilities, invests the capital, and tries to earn more on the assets than it owes on the liabilities.

This is why insurance can be powerful inside Brookfield.

The capital is long term. Brookfield has a large asset management platform. BAM can manage the insurance assets. Brookfield can invest in private credit, infrastructure debt, real estate debt, and other income-producing assets where it believes it has an advantage.

At the end of 2025, Brookfield Wealth Solutions had $143B of insurance assets and $1.9B of annualized cash flows. In Q1 2026, after the Just Group acquisition, insurance assets increased to about $180B.

The business targets a 15% return on equity.

The opportunity is clear. If Brookfield can scale insurance assets and invest them safely, Wealth Solutions becomes another large source of cash flow.

The risk is also clear. Private equity-backed insurance has attracted more scrutiny. Regulators are watching duration matching, liquidity, related-party activity, and how much insurance capital gets invested into affiliated private funds.

Our read is that Brookfield’s insurance business looks more conservative than many headlines suggest. The liabilities are long duration and more predictable than demand deposits. The company also says it holds large amounts of liquid assets.

The risk still deserves attention because this business depends on trust, regulation, and asset quality.

The operating businesses are lower-margin and more capital intensive than asset management. They also give Brookfield something many asset managers do not have: operating knowledge.

Brookfield buys assets, runs them, improves cash flows, refinances when appropriate, sells mature assets, and redeploys the proceeds.

That operating culture is the part of Brookfield that investors either love or struggle to underwrite.

How Brookfield makes money

Brookfield makes money through recurring fees, investment income, insurance spread, distributions, carried interest, and asset sales.

The asset management fee stream is the easiest to understand. If BAM manages $614B of fee-bearing capital, it charges fees on that capital. As fee-bearing capital grows, fee-related earnings should grow too, assuming fee rates and margins hold.

Carried interest is less predictable. Brookfield earns carry when fund returns pass agreed thresholds. This can become very large, but it depends on asset sales, fund performance, market liquidity, and timing.

Insurance spread is another earnings stream. Brookfield Wealth Solutions takes in retirement and insurance capital, owes a cost on that capital, and invests the assets to earn a higher return. The spread is profit.

Operating distributions come from Brookfield’s stakes in BIP, BEP, BBU, and real estate. These cash flows are often linked to contracted or inflation-linked revenues.

Asset sales are the fifth source.

Brookfield buys assets, improves them, and sells mature assets when the market price is attractive. In Q1 2026, Brookfield executed $17B of asset sales across the business. The company said substantially all sales were completed at or above carrying values.

This is one of the most important tests of the Brookfield story.

Skeptics often argue that private asset managers may overstate asset values. Brookfield’s answer is simple: when it sells assets, it aims to sell them at or above the values carried in its books.

That does not remove the need for skepticism. It gives investors a real test to monitor.

Why Brookfield is hard to copy

Brookfield’s moat does not come from one asset, one fund, or one famous deal.

It comes from the combination of scale, trust, operating knowledge, long-duration capital, and the ability to move capital across different parts of the group. That is why Brookfield is difficult to analyze. The same structure that creates the advantage also creates the complexity.

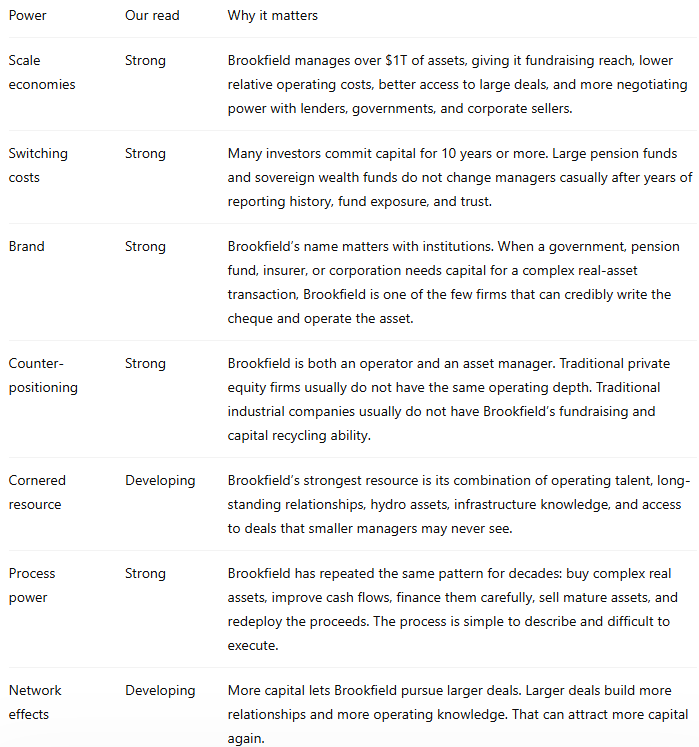

The BE Invested Labs 7 Powers review rates Brookfield’s moat as Wide and its moat trend as Strengthening. We agree with that assessment, with one condition: the moat depends on Brookfield continuing to allocate capital well.

If BAM’s returns weaken for a long period, the whole structure becomes less powerful.

Here is how the 7 Powers framework applies to Brookfield.

The strongest powers are scale, switching costs, brand, counter-positioning, and process power.

Scale matters because Brookfield can do transactions that smaller firms cannot fund or operate. A $30B infrastructure strategy changes the types of assets Brookfield can pursue and the type of counterparties it can sit across from.

Switching costs matter because Brookfield’s customers are pension funds, sovereign wealth funds, insurance companies, endowments, foundations, family offices, and other institutions that think in decades. If Brookfield performs, those investors often come back for the next fund.

Brand matters because the assets are complex. A government selling infrastructure, a company looking for a partner, or a pension plan allocating billions wants a manager that can survive a bad cycle. Brookfield’s history helps it raise capital even when headlines around private markets are negative.

Counter-positioning matters because Brookfield sits between 2 worlds. It has the investment platform of a large asset manager and the operating culture of a company that owns physical assets. That is rare. A financial sponsor can copy the language, but building the operating depth takes years. An industrial company can own assets, but raising and recycling third-party institutional capital is a different discipline.

Process power may be the most important one. Brookfield’s best deals are usually not based on buying something and waiting for a higher multiple. The best examples involve improving cash flows. Westinghouse, Clarios, toll roads, ports, rail, renewable power, and infrastructure assets all show the same pattern: Brookfield wants to buy assets where operational decisions can change the economics.

This is also where the risk sits.

The moat is only useful if Brookfield keeps using it properly. Scale can become a burden. Complexity can hide mistakes. Internal capital movement can create conflicts. Large funds can make it harder to find high-return deals. The more capital Brookfield manages, the more discipline it needs.

That is why we do not treat the moat as a free pass.

Brookfield has earned a premium because the track record is real. It still needs to prove that the same method can work at a much larger scale, inside a more complex structure, with higher interest rates and more scrutiny on private markets.

That is the Brookfield trade-off: a wide moat, a trusted management team, and a structure that still requires investors to keep asking hard questions.

Famous investment moves

The moat becomes easier to understand when you look at the deals.

Brookfield’s reputation was built through transactions where the company bought complicated assets, improved operations, and returned capital through sales, refinancings, or distributions.

Oaktree

The Oaktree deal was one of the most important moves in Brookfield’s modern history.

Brookfield bought a majority stake in Oaktree in 2019. Oaktree brought distressed credit, opportunistic credit, and the Howard Marks and Bruce Karsh reputation into the Brookfield group.

That deal mattered because credit is now one of the largest growth areas in alternatives. Oaktree also gave Brookfield deeper access to private credit, distressed debt, and dislocation opportunities.

In 2025, Brookfield agreed to acquire the remaining Oaktree stake for about $3B, making Oaktree even more central to Brookfield’s credit strategy.

For investors, Oaktree matters because it gives Brookfield another way to profit when markets become stressed.

Westinghouse

Brookfield acquired Westinghouse out of bankruptcy in 2018.

The thesis was that Westinghouse’s fixed-price nuclear construction problems had hidden a valuable nuclear services business. The core business served the installed nuclear fleet with fuel, maintenance, and services.

According to the research pack, Brookfield worked with the Westinghouse team, made add-on acquisitions, improved cash flows, and later sold the business at an implied enterprise value of around $8B. The reported result was roughly 6x invested capital and an IRR around 60%.

That is the Brookfield method in one example: buy when a good business is hidden inside a bad situation, fix the structure, improve cash flows, then sell when the market appreciates the asset.

Clarios

Brookfield acquired Clarios from Johnson Controls in 2019.

Clarios makes automotive batteries. The business had a long operating history, large scale, and exposure to replacement battery demand. The BE Invested research pack describes it as one of Brookfield’s most documented operational transformations.

Brookfield improved operations, reduced debt, and increased cash generation. The research pack says Brookfield later refinanced the business and received a $4.5B special distribution while still owning the equity interest.

That matters because it shows the business can return capital before a full exit.

Infrastructure assets

Brookfield has also created value through rail, ports, toll roads, pipelines, data infrastructure, telecom towers, and renewable power.

The research pack gives examples such as Australian rail expansion, Chilean toll roads, and global toll road operations where Brookfield created value through capacity additions, traffic growth, contract wins, and better cost management.

These examples are less glamorous than AI or semiconductors. They are exactly the type of assets Brookfield likes.

They produce cash. They require operating skill. They can use debt responsibly if cash flows are predictable. They can become more valuable when cash flows grow.

The financial picture

Brookfield’s financials require care because GAAP earnings do not fully explain the business.

The company focuses heavily on Distributable Earnings, or DE. Brookfield uses DE to show the earnings available for distribution to shareholders, built from asset management earnings, wealth solutions earnings, operating business distributions, realized carried interest, and disposition gains.

This metric is useful because Brookfield is a capital allocation business.

It is also a management-defined non-IFRS metric. Investors need to understand what is included, what is excluded, and how much judgment sits inside the number.

Here are the latest headline numbers we are using:

The financial picture is strong if you accept Brookfield’s DE framework.

Brookfield has growing fee-related earnings, a large insurance asset base, large deployable capital, and active asset sales. It is also repurchasing shares when management believes the stock trades below intrinsic value.

In Q1 2026, Brookfield repurchased $470M of BN shares at an average price of $41 and $575M of BAM shares.

Management said the BN repurchases were done at roughly a 40% discount to its view of intrinsic value at quarter end, which management estimated at $66 per share.

That is an important data point.

Our BE Invested Labs model is more conservative. It estimates fair value at $48. The difference comes from Brookfield management valuing the business from inside the system and our model applying a higher discount for complexity, leverage, and credit risk.

The bull case

The bull case is built on 5 points.

1. Brookfield has a long record of capital allocation

Brookfield says shareholders have earned 19% annual compound returns over more than 30 years.

That record matters. Few companies can point to multiple decades of strong returns through different interest rate regimes, crises, real estate cycles, credit cycles, and market crashes.

Bruce Flatt and the Brookfield team have earned the right to be taken seriously.

2. The assets are in demand

Brookfield focuses on assets tied to infrastructure, energy, data centers, transmission, real estate, credit, renewable power, nuclear services, and essential operating businesses.

The AI infrastructure theme is especially important now.

AI needs data centers. Data centers need power. Power needs generation, storage, transmission, land, cooling, financing, and operators that can work across governments, utilities, hyperscalers, and capital markets.

Brookfield has exposure across several of those pieces.

This is why management keeps talking about digitalization, decarbonization, and deglobalization. The language can sound corporate, but the underlying asset need is real.

The world needs more power, more grid capacity, more data infrastructure, more private capital, and more complex financing.

Brookfield has built a business around those needs.

3. BAM is still growing

Brookfield Asset Management is the center of the thesis.

Fee-bearing capital reached $614B in Q1 2026, up 12% year over year. Fee-related earnings increased 11% in the quarter.

That is important because the market often fears that large asset managers eventually run out of runway. Brookfield’s current numbers suggest the platform is still growing.

BAM also benefits from repeat capital.

Large pension funds, sovereign wealth funds, insurance companies, and institutions tend to re-commit to managers that perform well and treat them fairly. This creates long-term relationships that are difficult for smaller managers to copy.

4. Insurance can add another earnings base

Brookfield Wealth Solutions is becoming more important.

After Just Group, insurance assets increased to about $180B. Brookfield wants to combine BN and BNT into a larger insurance and investment organization.

The bull case is that insurance gives Brookfield a large base of long-duration capital. BAM can manage the assets. BWS can earn spread. BN can use the combined capital base to support growth.

This could make Brookfield look more like a mix of asset manager, insurer, and real-asset investor.

If it works, the market may value BN with less of a conglomerate discount.

5. Asset sales support the marks

Brookfield had a record year for asset sales in 2025, and Q1 2026 stayed active with $17B of asset sales.

The company says substantially all Q1 sales were completed at or above carrying values.

For a private asset manager, this matters. The quality of marks is tested when assets are sold. If Brookfield keeps selling assets at or above carrying values, the bear argument around inflated private marks becomes harder to defend.

This is one of the most important monitoring points for BN.

The bear case

The bear case is not about Brookfield being a bad business.

It is about the risks that come with the model.

1. The structure is extremely complex

Brookfield has asset management, insurance, operating businesses, listed affiliates, private funds, internal capital commitments, direct investments, public stakes, carried interest, and real estate holdings.

Capital can move between entities. One Brookfield entity can manage capital for another Brookfield entity. BN can invest into BAM funds. BWS can allocate assets to Brookfield-managed strategies. Operating businesses can use capital sourced from Brookfield’s broader system.

This structure can create advantages.

It can also make the business difficult to analyze from the outside.

Public investors have to trust that capital is being allocated fairly, reported properly, and managed with long-term discipline.

2. Distributable Earnings needs trust

DE is the main metric for BN.

It is also a non-IFRS metric. Brookfield defines it. Brookfield reconciles it. Brookfield uses it to explain the business.

We understand why DE matters. GAAP earnings can be noisy for a business that owns assets, sells assets, consolidates some businesses, equity accounts others, and holds unrealized gains.

Still, investors should not outsource judgment.

The useful way to read BN is to track DE, fee-related earnings, realized carry, asset sales, cash flow, liquidity, and debt together.

DE alone is too clean for a company this complex.

3. The debt story needs careful interpretation

Brookfield’s consolidated debt looks massive.

The key defense is that much of it is non-recourse, asset-level financing. That means a problem at one asset should not automatically become a claim on the parent company.

That structure has worked over time.

The risk is a systemic credit event. If refinancing markets freeze, commercial real estate values fall, and lenders demand more equity, Brookfield may have to choose between walking away from assets, injecting capital, or accepting lower returns.

Brookfield has significant liquidity and long-dated corporate debt. Q1 2026 disclosures show $188B of deployable capital and a 15-year weighted-average term on corporate debt.

That helps.

The risk does not disappear. The business is still sensitive to rates, credit spreads, refinancing markets, and asset values.

4. Real estate has already shown stress

Brookfield’s real estate business has had public office defaults in recent years.

The company’s response is that a large property portfolio will always have weaker assets during stressed markets. It is also shifting its real estate exposure toward what it considers the best assets and reducing some cyclicality over time.

Q1 2026 data showed strong occupancy in super core and core plus assets, and a successful $1.9B refinancing of Two Manhattan West.

That is a positive sign.

The real estate issue is still worth watching. Office, retail, refinancing rates, tenant demand, and asset sales all matter.

5. The whole thesis depends on BAM’s future returns

This is the biggest risk.

Brookfield’s insurance profits depend on how the capital is invested. BN’s retained cash flows are reinvested into the system. Carried interest depends on fund performance. BAM’s fee growth depends on investors trusting the platform and committing more capital.

If BAM stops producing strong returns, the entire system slows down.

That is why BN is ultimately a bet on capital allocation.

Brookfield can own the right asset classes, attract the right clients, and raise the right funds. The value still depends on buying well, financing well, improving operations, and selling well.

Valuation

The BE Invested Labs platform rated BN as Neutral.

The fair value estimate is $48 per share.

The platform’s conclusion is not bearish.

It says the current price does not offer a large enough margin of safety for the risks.

This is where our view lands too.

Brookfield is a high-quality business with a long runway, strong management, and exposure to real assets that should matter more over time. It also requires more trust than the average public company.

If the stock trades at a large discount to a conservative view of intrinsic value, the complexity becomes easier to accept. If it trades close to fair value, the investor is being paid less for taking on that complexity.

That is the difference between liking the business and liking the price.

What we are watching

Brookfield is measurable if you focus on the right items.

For us, the most important numbers are fee-related earnings, DE before realizations, asset sales versus carrying value, and parent-level liquidity.

If those remain strong, the Brookfield thesis is intact.

If those weaken together, the bear case gets louder.

Our view

Brookfield is one of the rare companies where the business quality is clear and the structure still demands caution.

We respect the track record. We respect Bruce Flatt. We respect the owner-operator culture. We respect the fact that large institutions keep giving Brookfield more capital. We also respect the fact that public investors should not blindly accept management-defined metrics from a complex investment company.

The BE Invested Labs research platform lands on Neutral, with a $48 fair value estimate.

Our qualitative view is more positive on the long-term business than the rating may sound. Brookfield is probably one of the better ways to get exposure to real assets, private markets, infrastructure, energy demand, AI infrastructure, and long-term capital allocation.

The valuation view is more restrained.

BN is not a simple compounder. It is a complex compounder.

The business can work very well for patient investors if BAM keeps producing strong returns and management keeps simplifying the structure. The same complexity can punish investors if credit markets turn, real estate stress grows, or the market loses trust in DE and private asset marks.

That is the Brookfield debate.

The company is good. The current price needs more margin of safety.

Our answer: close, but not enough to call it compelling.

Use BE Invested Labs to generate structured company research, valuation notes, bull and bear cases, and AI audio briefings.

Subscribe to BE Invested Labs for more business breakdowns like this.

— Buyce & Emmanuel, BE Invested Labs

References and data notes:

BE Invested Labs Master Synthesis report

Disclaimers & Disclosures

AI Transparency: BE Invested Labs uses AI to aggregate financial data and format reports. The AI structures the information. Users determine their own investment thesis, risk management, and market outlook. We audit the system outputs to reduce AI errors. We use these exact reports to manage our own capital.

Legal Disclaimer: This platform provides educational and informational content. BE Invested Labs is not a registered investment advisor and does not provide financial, investment, tax, or legal advice.

This Brookfield breakdown took many hours of reading, checking, and simplifying because BN is easy to respect but hard to understand.

We hope it helps you appreciate the business Brookfield has built, the value it brings as a real-asset allocator, and the risks investors still need to watch.

Thanks for reading. We’d love your thoughts and pushback.