Business Breakdown: ASML — The Forty-Year Bet That Won

BE Invested Labs | Buyce & Emmanuel | June 2026 Read time: ~18 minutes. Disclaimer: we own positions in this company.

ASML is one of those companies that sounds boring until you understand what it controls.

The company makes lithography machines. These machines print circuit patterns onto silicon wafers. Without lithography, there are no advanced chips. Without advanced chips, there is no serious AI infrastructure, no high-end GPUs, no advanced smartphones, no leading-edge data centers, and no continued push toward smaller, faster, more efficient semiconductors.

That is the simple thesis.

ASML sits in one of the most important parts of the semiconductor manufacturing chain. Its EUV machines are used to produce the most advanced chips in the world, including the chips needed for AI, high-performance computing, advanced memory, and next-generation logic nodes.

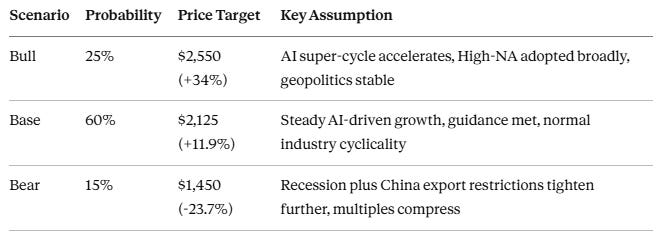

The BE Invested Labs ASML report gives the company an Outperform rating, with a probability-weighted fair value estimate of $2,150 per share. At the report price of $1,899.48, that implies around 13.2% upside over a 12 to 24 month horizon. The bull case reaches $2,550. The bear case falls to $1,450.

That range matters.

ASML is a very high-quality company. It is also expensive. The investment debate is not whether ASML is important. The debate is whether today’s valuation still leaves enough room for future returns.

If you want business breakdowns like this in your inbox, subscribe to BE Invested Labs. We break down companies through history, numbers, valuation, risk, and long-term business quality.

Prefer to listen? We generated an AI audio briefing from the full BE Invested Labs ASML research report.

From a leaky shed to the center of the chip industry

ASML started in 1984 as a joint venture between Philips and ASM International. It began life in a leaky shed near Philips’ buildings in Eindhoven, the Netherlands.

That detail matters because ASML was not born as an obvious winner. It was a small Dutch lithography company entering a market with bigger competitors, limited customers, and expensive research needs. ASML’s own history says the company had few customers in the late 1980s and could not stand on its own feet. ASMI withdrew, Philips was cutting costs, and the young company’s future was uncertain.

So before ASML became a European technology giant, it nearly failed.

The first real escape came in the 1990s with the PAS 5500 platform. That system helped ASML win important customers, improve productivity, and move toward profitability. In 1995, ASML became a public company listed in Amsterdam and New York. Philips sold half its stake at the IPO and later sold the rest.

The early 2000s then gave ASML another push. In 2001, the company introduced TWINSCAN, a dual-stage lithography system that could expose one wafer while measuring and aligning another. That improved productivity for customers. In 2003, ASML introduced its first immersion lithography machine. By 2007, it had shipped an immersion system with a numerical aperture of 1.35, the highest in the industry at the time.

This period matters for investors because ASML did not win by accident. The company kept solving specific customer problems: resolution, productivity, throughput, cost per chip, and manufacturing accuracy.

Those wins made ASML stronger before EUV became commercially real.

The EUV bet

EUV stands for extreme ultraviolet. ASML’s EUV systems use light with a wavelength of 13.5 nanometers, which is almost in the x-ray range. That shorter wavelength allows chipmakers to print extremely small and complex layers on advanced chips.

This technology took more than 2 decades to develop. ASML says it invested more than €6 billion in EUV R&D over 17 years. The company also acquired Cymer in 2013 to strengthen its EUV light source capability.

The technical problem was brutal. EUV light is absorbed by air, so the system must operate in a vacuum. The light source fires laser pulses at droplets of tin up to 50,000 times per second. The wafer stage positions wafers within a quarter of a nanometer and checks or adjusts 20,000 times per second.

That is why EUV became a graveyard for competitors.

Many companies explored EUV. ASML kept going. In 2006, it shipped the first EUV demo tools. In 2010, it shipped the first pre-production EUV system. In 2013, it shipped the first production EUV system. In 2016, customers began ordering the NXE:3400 in higher volumes. At the start of 2020, ASML celebrated the 100th EUV system shipment.

The timing is important. ASML did not suddenly become central to AI because of Nvidia headlines in 2023 or 2024. The company had already spent decades building the technology that AI now depends on.

There is a temptation to tell the EUV story as a simple genius bet that obviously paid off. That is too clean. EUV was expensive, slow, technically painful, and commercially uncertain for years. ASML needed deep customer support to keep pushing. In 2012, Intel, TSMC, and Samsung joined ASML’s customer co-investment program to help fund EUV and other next-generation work.

That was the important signal.

ASML’s biggest customers were willing to fund the company because their own futures depended on the technology.

Why EUV changed the economics

A normal equipment supplier sells machines and waits for the next order cycle.

ASML’s EUV business has different economics because customers build multi-billion-dollar fabs around its tools. Once a leading-edge chipmaker commits to an ASML-based process, the relationship can last for decades through service, software, upgrades, field options, and future tool generations.

The machine sale is only the beginning.

ASML calls its service and upgrade revenue Installed Base Management. In Q1 2026, Installed Base Management sales were €2.488 billion, up from €2.134 billion in Q4 2025. That is a large business inside the business. It matters because every machine shipped can create future service and upgrade revenue.

This is part of why ASML deserves a premium valuation.

The company sells some of the most complex machines in the world to a small group of customers that cannot easily replace it. TSMC, Samsung, Intel, SK Hynix, Micron, and other major chipmakers do not buy ASML systems casually. They buy them because their roadmaps require them.

The customer list is concentrated, which creates risk. The same concentration also shows how hard the market is to enter. Only a small number of companies can afford leading-edge fabs. Those companies need the best lithography tools available.

At the leading edge, ASML is the supplier.

High-NA EUV and the next technical record

The next phase is High-NA EUV.

ASML’s current NXE EUV systems use a numerical aperture of 0.33. The newer EXE systems use High-NA technology with a numerical aperture of 0.55. ASML says the EXE platform prints with 8 nm resolution and is designed to support sub-2 nm logic and leading-edge DRAM nodes.

The first High-NA EUV system was delivered in December 2023. ASML expects the platform to support process development and high-volume manufacturing in 2025 to 2026.

This matters because High-NA can increase ASML’s revenue per system and extend its leadership into future chip nodes. The BE Invested Labs report models High-NA as one of the main drivers of future growth and margin expansion. The report’s bull case assumes faster High-NA adoption, strong AI-driven demand, and operating margin expansion toward 45% by 2030.

The technical risk is still there. High-NA systems are expensive. Customers need to justify the economics. The semiconductor industry may use advanced packaging and chiplet designs to improve performance in ways that reduce pressure to shrink everything at the same pace.

Still, the commercial incentive remains clear. AI workloads require more compute. More compute requires more advanced chips. Advanced chips require advanced manufacturing. ASML’s tools sit inside that chain.

The Business Model: Two Revenue Streams, One Relationship

ASML’s revenue comes from two places.

Net System Sales is the headline number — selling new lithography machines to chipmakers. These are not simple transactions. A single fab build can involve multi-year planning cycles, technical integration, and machine orders that commit customers years in advance. ASML regularly receives large down payments before machines are even delivered, which is why the company can occasionally show strong cash generation even in quarters where formal revenue recognition is lower.

Installed Base Management is the second stream, and it is the one that gives ASML a quality that pure equipment suppliers rarely have. This covers service contracts, hardware upgrades, and software updates for the thousands of ASML systems already in operation. It is recurring, high-margin, and grows automatically as more machines get deployed. It also means that once a customer buys an ASML system, the relationship does not end at the purchase. It compounds for decades.

This is a meaningful distinction from a typical capital equipment company. ASML is not just selling machines. It is building a permanent, recurring revenue stream on top of every machine it has ever shipped.

The Moat: Why Nobody Can Catch Them

ASML did not become a monopoly by accident. It took decades of accumulated advantage to reach a position where no competitor can credibly enter their core market.

Scale is a barrier nobody can replicate. The R&D required to develop EUV technology cost billions over multiple decades. ASML is the only company that spread that cost across the entire global market for advanced chips. A new entrant would need to spend similarly — and then win customers away from a supplier with 30+ years of integration into their fabs. That is not a business decision any competitor has been willing to make. Nikon and Canon tried, and fell behind, not because they lacked ambition, but because the physics and the capital requirements were simply too hard.

Switching costs are among the highest of any industry. Swapping out a lithography supplier is not a software upgrade. It means redesigning fab processes, retraining engineers, renegotiating supply chains, and accepting years of yield risk during the transition. Customers like TSMC and Samsung have built their most advanced production lines entirely around ASML’s technology. They do not swap suppliers. They deepen the relationship.

The supply chain is cornered. ASML sources light sources from a single German supplier, Trumpf. Their optics come primarily from Zeiss, where ASML owns a 24.9% stake. They have effectively secured exclusive or near-exclusive access to the components needed to build these machines. A competitor could not simply set up a production line — the raw inputs are controlled.

The installed base creates compounding lock-in. Every system shipped adds to a recurring revenue base. Every upgrade cycle reinforces integration. Every new fab build starts from the assumption that ASML machines will be inside it.

The BE Invested report rates ASML’s moat as Wide, with a trend of Strengthening. The introduction of High-NA EUV extends the technological frontier further out of reach for any would-be competitor. The next generation is more complex, more expensive, and more deeply integrated into customer roadmaps. The moat does not just hold — it widens with every product cycle.

The numbers before and after the inflection

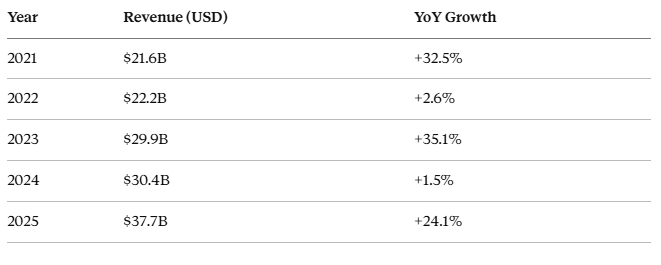

ASML was growing consistently even before the AI era reshaped demand.

Revenue moved from €18.6 billion in 2021 to €35.3 billion in 2025, a 5-year CAGR of 18.8% in USD terms. The one soft year was 2024, where revenue dipped slightly as customers worked through inventory. Then 2025 came in at $37.67 billion, up 24.1%.

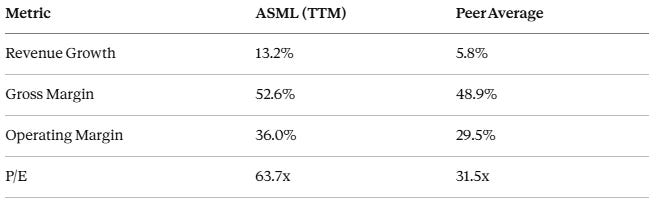

Gross margin has held above 50% through supply chain disruptions, inflation, and two years of softer chip demand. It currently sits at 52.6% on a trailing twelve-month basis. Operating margin is 36.0%, up from 30.7% three years ago. Net income for the trailing twelve months is $10.01 billion.

The peer group — Applied Materials, Lam Research, KLA Corporation, and Tokyo Electron — averages TTM revenue growth of 5.8%. ASML is growing at 13.2% TTM.

The balance sheet is genuinely strong. ASML holds $8.38 billion in cash against $2.71 billion in debt, making it a net cash position of $5.67 billion. Free cash flow is $8.97 billion. The company returned approximately €8.5 billion to shareholders in 2025, through a combination of dividends and buybacks. It could repay its entire debt load from a single quarter’s net income.

ROIC sits at 26.1% against a WACC of roughly 8-11%. That 1,500 to 1,800 basis point spread is the quantitative proof that the moat is real.

The bull case: AI has changed the demand structure

The specific argument here is not just that AI demand is growing. It is that AI requires leading-edge chips at a volume and complexity the world has never produced before, and every one of those chips can only be manufactured using EUV.

Hyperscalers — Microsoft, Google, Amazon, Meta — have made capital expenditure commitments measured in hundreds of billions of dollars per year. That spending goes into data centres, training clusters, and inference infrastructure. All of it runs on advanced silicon. All of that silicon requires EUV.

The semiconductor sovereignty dynamic adds another layer. The US CHIPS Act, Europe’s Chips Act, Japan’s subsidies for TSMC’s domestic fab, and Intel’s domestic expansion are all government-funded programmes to build new advanced manufacturing capacity. Every new fab being built in the western world is a new ASML customer.

High-NA EUV is just starting its adoption cycle. The first EXE systems are shipping now. Every major chipmaker will need to transition to this platform to stay competitive at the leading edge. That cycle will run for years and generate revenue at $350-380 million per machine.

CEO Christophe Fouquet, on recent earnings calls, has described demand as “unprecedented” and confirmed the company is sold out for 2026. The company’s problem, he says, is not finding demand. It is building enough machines to meet it.

Management’s 2030 guidance — €44 to €60 billion in revenue — implies a continuation of the growth rate they’ve been delivering for a decade.

The bear case: premium multiples and real risks

ASML trades at 63.7x trailing earnings and 57.2x EV/EBITDA. Peers trade at 31.5x and 22.1x respectively. ASML commands roughly a 100% premium to peers on both metrics.

That premium is defensible, as explained above. A monopoly on the only technology that can produce leading-edge chips justifies pricing well above commodity equipment suppliers. But the premium also means any negative surprise hits hard. There is no valuation cushion here.

China is the live risk. China currently accounts for roughly 26% of ASML’s revenue, predominantly from older DUV machines. ASML has been barred from shipping EUV to China since 2019 due to Dutch and US export controls. If those controls expand further to include DUV systems, the revenue impact would be immediate and significant. Management acknowledges this as the most actively monitored risk in the business.

Geopolitics in Taiwan is the tail risk. TSMC is ASML’s largest customer. TSMC’s primary manufacturing is in Taiwan. A military or political crisis affecting Taiwan would cascade directly through ASML’s order book. This is a low-probability, high-severity scenario that the market intermittently reprices. It has not gone away.

The terminal risk is the end of Moore’s Law economics. EUV machines cost over $200 million. High-NA systems are approaching $380 million. At some point, the cost of transitioning to a new process node may no longer be justified by the performance gain. If chipmakers shift to alternative approaches like advanced packaging and chiplets to improve performance rather than shrinking transistors further, demand for the most advanced EUV systems could flatten. This is a long-duration risk, not an imminent one, but long-term holders should keep it in mind.

Customer concentration is real. Over 80% of revenue comes from 3 customers. A serious strategic or financial problem at TSMC, Samsung, or Intel would show up immediately in ASML’s order book.

The bear case price target from our engine is $1,450, representing 23.7% downside from current levels. It requires a confluence of negative events — recession, export restriction escalation, and multiple compression — to materialise simultaneously. Possible. Not probable.

Forensic: what the accounting tells us

Our engine’s forensic review found no signs of earnings manipulation. Cash conversion is strong: operating cash flow of $10.53 billion against net income of $10.01 billion gives an OCF/Net Income ratio of 1.05x, confirming that reported profits are translating directly into cash.

One yellow flag worth watching: ASML capitalises a portion of development costs under IFRS. In the first half of 2025, €473.9 million was capitalised. This is a compliant accounting practice, but it boosts current-period net income by removing certain R&D costs from the income statement. If the rate of capitalisation accelerates sharply relative to total R&D spend, it would be worth investigating.

Working capital can swing significantly due to large customer down payments and the timing of machine deliveries. In 2023, net profit grew 27% while operating cash flow fell 31% — a divergence caused by working capital movements, not a business problem. That has since normalised.

No significant off-balance sheet liabilities. Inventory days are elevated at approximately 218-319 days, reflecting the complex production cycle, but this is structural. ASML often collects down payments before delivery, giving it a cash position that runs ahead of its production commitments.

What the BE Invested Labs engine concluded

Our engine initiated coverage of ASML with an Outperform rating and a probability-weighted fair value of $2,150 per share.

Current price at time of report: $1,899.48. Implied upside: 13.2%.

The 3 scenarios:

The DCF model assumes 15% revenue CAGR through 2030, a terminal growth rate of 3.5%, and a WACC of 8-11%. Management’s own guidance for 2030 is €44 to €60 billion in revenue, with gross margins of 56-60%. Those targets look achievable given the trajectory.

The bull case for margin expansion is grounded in product mix. High-NA EUV systems, at $350-380 million per unit, carry gross margins expected north of 60%. As those units grow as a share of revenue, they mechanically pull the corporate average up from 52.6% toward the 56-60% range management is guiding. Installed Base Management also carries margins above the corporate average, and that segment is growing faster than total revenue.

Management and governance

Christophe Fouquet became ASML CEO in April 2024 after more than 15 years inside the company. He previously led key technology and business areas, including the EUV business. That gives ASML leadership continuity after the Peter Wennink era.

This matters because ASML is not a normal sales organization. The CEO needs to understand physics, customers, geopolitics, supply chains, government restrictions, long-term R&D, and capital allocation.

The BE Invested Labs report gives Fouquet an A- management assessment. The main reason is his technical background and long operating history within ASML. His shorter time as CEO means investors should keep watching execution, but the transition looks orderly.

Governance looks clean overall. ASML has a Dutch two-tier board structure, with a Board of Management and an independent Supervisory Board. The report found no major governance red flags such as dual-class shares, poison pills, or problematic related-party transactions.

Capital allocation also looks sensible. ASML invests heavily in R&D, maintains a strong balance sheet, pays dividends, and repurchases shares. In 2025, it returned €8.5 billion to shareholders.

For a company with this much technical risk and geopolitical pressure, that financial strength matters.

Our view

We hold ASML in our own portfolios. ASML is one of the few companies in the world where, if you understand the business, the investment case is not complicated. It is the only supplier of the technology that makes advanced chips possible. The demand for those chips is growing because AI is growing. AI is not going away.

Our BE Invested Labs engine rates it Outperform, with a probability-weighted target of $2,150.

Current price is $1,899. That is 13.2% upside to fair value, with a bull case of $2,550 if AI adoption accelerates faster than expected. The bear case of $1,450 requires specific negative events to coincide.

The entry zones from our report are around the $1,750 to $1,900 range for a measured position, with more aggressive adding below $1,600. We see the current price as a fair entry for a long-duration compounder, with particular strength if there is any macro-driven pullback.

One governance note worth holding: total insider ownership at ASML is estimated at roughly 0.02% of the company. There is no meaningful open-market buying by the executive team. The absence of a large personal stake does not impair our thesis — management’s actions have created immense shareholder value — but it is a data point we note for anyone who values owner-operator alignment as a signal.

What would make you more cautious on ASML: valuation, China restrictions, Taiwan risk, or the cost of High-NA adoption? Reply in the comments. We want this series to be useful, but also debatable.

The metrics to track quarterly:

EUV system bookings: above €7B per quarter is a thesis upgrade signal; below €4B for 2 consecutive quarters is a concern

Gross margin: sustained above 54% is a positive signal; sustained below 48% raises questions about mix and pricing

Inventory days: currently 218-319 days; watch for a sustained trend toward 300+ days

China revenue percentage: currently approximately 26%; any abrupt policy-driven drop signals immediate downside risk

High-NA order announcements: firm orders from all 3 key customers (TSMC, Samsung, Intel) would be a meaningful thesis upgrade

ROIC: currently 26.1%; a sustained drop below 25% would flag deterioration

The company that started in a shed in Veldhoven, that nearly went bankrupt pursuing a technology most competitors abandoned, that had to be rescued by its own customers in 2012, is now the single most important supplier in the global semiconductor supply chain.

That is not a narrative. That is forty years of compounding decisions that turned out to be right.

If you know someone studying semiconductors, AI infrastructure, or European compounders, share this breakdown with them.

Try the BE Invested Labs platform here: beinvestedlabs.com

If research like this is useful, subscribe to BE Invested Labs.

— Buyce & Emmanuel, BE Invested Labs

Disclaimers & Disclosures

AI Transparency: B.E Invested Labs uses AI to aggregate financial data and format reports. The AI structures the information. Users determine their own investment thesis, risk management, and market outlook. We audit the system outputs to reduce AI errors. We use these exact reports to manage our own capital.

Legal Disclaimer: This platform provides educational and informational content. B.E Invested Labs is not a registered investment advisor and does not provide financial, investment, tax, or legal advice.

References and data notes

ASML Q1 2026 results were cross-checked against ASML’s official press release: €8.8 billion net sales, 53.0% gross margin, €2.8 billion net income, Q2 2026 sales guidance of €8.4 billion to €9.0 billion, and full-year 2026 sales guidance of €36 billion to €40 billion.

ASML 2025 full-year figures were cross-checked against the official ASML 2025 Annual Report page: €32.7 billion net sales, 52.8% gross margin, €9.6 billion net income, €24.73 basic EPS, 535 total systems sold, including 48 EUV systems.

ASML EUV and High-NA technology descriptions were cross-checked against ASML’s official EUV product page.

ASML 2030 revenue and gross margin targets were cross-checked against ASML Investor Day materials and Reuters reporting on ASML’s 2024 Investor Day.